Exiting these Saba trust targets? Here are some fresh ideas

Kepler share options for investors exiting Edinburgh Worldwide and Impax Environmental Markets, or for those simply with cash to put to work.

27th March 2026 14:02

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

The timetables are now set for Edinburgh Worldwide Ord (LSE:EWI) and Impax Environmental Markets Ord (LSE:IEM)’s exit tender offers. EWI shareholders must vote for (or against) the tender offer by 8 April 2026, and if the tender passes, must vote to tender their shares by 16 April 2026, although some platforms may have earlier deadlines. Baillie Gifford is maintaining a micro-site at www.trustewit.com, which should host any updates. For IEM, the relevant dates are 16 April 2026 and 17 April 2026, with the details in the circular.

One way or another, these strategies will disappear from the investment trust sector, taking two distinctive funds out of the game. It could even end up being a decent time to be receiving a slug of cash back, if the war in the Middle East continues to escalate and we see a major sell-off.

Here are a few options investors might like to consider in different areas, depending on what they held the trusts for in the first place.

The smaller company options

Both EWI and IEM have smaller company tilts. After a long period in which large caps have outperformed globally, the number of small-cap options for investing outside the UK has declined. The Global Smaller Companies Trust Ord (LSE:GSCT) is the one truly global small-cap trust left. Manager Nish Patel covers the ground with the help of specialist regional managers at Columbia Threadneedle, some of whom run sleeves of stocks in their region of expertise. Nish takes a value-sensitive approach to regional allocation and has been underweight the US for some time. This could suit those investors keen to play the rotation out of that market we have been seeing post-tariff announcements. Nish thinks there have been some global factors weighing on the relative performance of small caps, and there is scope for these to reverse. GSCT is a more conventional small-cap trust than either EWI and IEM, so it could work well for those looking to take exposure to this out-of-favour factor, which has historically been a major source of active alpha.

One small-cap trust to have done very well recently is Aberdeen Asia Focus PLC (LSE:AAS). Under manager Gabriel Sacks, AAS’s small-cap portfolio has outperformed mainstream Asian markets over one- and three-year periods. In the recent volatility, the discount has widened out a bit to 11%, which could end up being an opportunity. It means narrowing your scope from the globe to just Asia, but with Asia such a significant part of global GDP and including many companies so central to key trends in technology, there is a lot to be said for overweighting this region.

The Baillie Gifford options

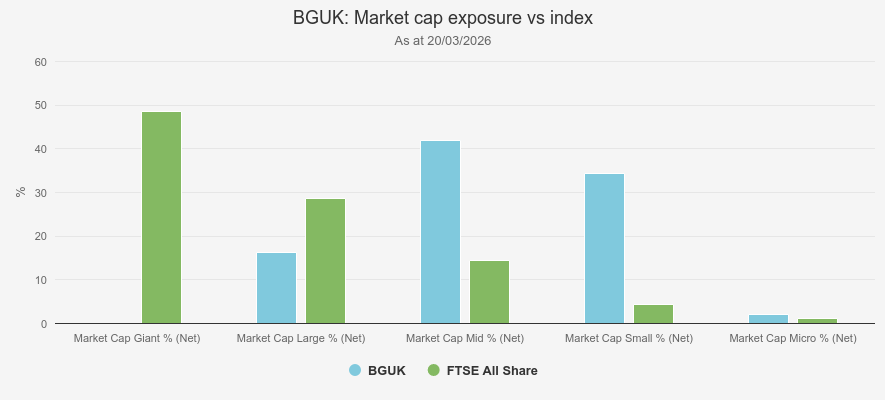

For those who want to keep some small-cap exposure while also retaining Baillie Gifford’s high growth investment approach, Baillie Gifford UK Growth Trust Ord (LSE:BGUK) could be worth a look. According to Morningstar data, BGUK has 34% in small caps and a further 42% in mid caps. We think UK SMIDs could be one of the next out-of-favour markets to see a rerating, with sentiment having become so poor that the only way is up. BGUK’s shares trade on a 10.4% discount to NAV. Games Workshop Group (LSE:GAW) is the top holding, while St James Place (SJP) also features in the top 10, it could be an interesting recovery play.

MARKET-CAP EXPOSURE

Source: Morningstar

Baillie Gifford Shin Nippon Ord (LSE:BGS) is entirely focused on smaller companies, those being in Japan. Performance has been disappointing for some time, but this has focused the attention of both board and manager on turning things around. Changes to the management team have been made, and the portfolio overhauled, and a tender offer has been made by the board, which has also highlighted that it will take further action as required. BGS is probably as out of favour as a strategy can be, which should pique the attention of contrarian and value investors.

The sustainability options

IEM’s departure means there are now no dedicated ESG/environmental equity trusts left. This speaks to a changing political climate, as well as a bursting of a 2021 bubble in certain sectors, which has left investors bruised. Net Zero by 2030 may have been finessed to ‘Net Nearly Zero by today plus 15 or 20 years’, but the social and political impetus to reduce emissions and encourage sustainable development hasn’t gone away, and remains important to many investors. One trust with a strong commitment to ESG in stock selection is Dunedin Income Growth Ord (LSE:DIG). This factor hasn’t been helpful to performance in the most recent reporting periods, but may well do so when the cycle turns. DIG has recently boosted its dividend to a minimum of 6% of NAV, paid from capital when necessary. For investors buying now, the c. 8.4% discount means the share price yield is higher too. We wrote a full update note on the trust in December.

One of the consequences of the war in the Middle East is to highlight how important energy security is, and having diverse sources of power, preferably those which aren’t dependent on that region. It’s hard to see how this doesn’t lead to renewed political impetus behind renewable power. Even before the war, the managers of BlackRock Energy and Resources Inc (LSE:BERI), who can invest across traditional energy and energy transition stocks, were telling us they were overweight renewables. Renewables are quick to build and connect to the grid, which makes them an obvious solution for governments wanting to quickly meet the expanding energy consumption needs of AI. We think energy security is another reason to favour renewables, and these two powerful factors could see Greencoat UK Wind (LSE:UKW) come back into favour. UKW is still on a discount of 23% at the time of writing, despite a sharp rise in the share price last week on expectations of higher electricity prices, which will feed through into the bottom line. The yield is an exceptional 10% at these levels, with higher electricity prices only going to improve dividend cover.

Conclusion

April is the cruellest month, which may mean it is the moment of maximum opportunity for investors. For humanitarian reasons, we hope the current conflict ends as quickly as possible, but sadly, a conclusion can’t be assured. For those receiving cash back from IEM and EWI’s exit tenders, it could be that they are faced with opportunities in significantly sold-off markets, which is potentially lucrative if you can force yourself to invest when the screen is red. Unsurprisingly, the departing trusts have a number of factor exposures which are out of favour: small cap, growth, and sustainability. For contrarians who have some cash to put to work, whether from the tenders or otherwise, this could be the time to allocate to these areas.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.