How to make early retirement a possibility

Achieving financial freedom before old age is becoming an increasingly difficult nut to crack, but all is not lost.

21st May 2026 15:01

by Craig Rickman from interactive investor

“For too many people, pension planning has remained an incomprehensible maze.”

This stinging assessment of the UK’s retirement savings framework was made back in 2002 by Baroness Hollis of Heigham, upon announcing the launch of Pension Simplification, also known as A-Day.

- Invest with ii: SIPP Account | Stocks & Shares ISA | See all Investment Accounts

This radical overhaul of the pension tax system took effect four years later, and despite the initiative’s best intentions, things remain a quagmire. A great deal has changed in the two decades since, but in many ways the labyrinth has become harder to navigate as key planning decisions can stretch years beyond the point you stop working.

One of the biggest cohorts impacted by the complexities are those seeking to retire early - a goal that may seem a pipe dream for many workers. And there are multiple other challenges that stand between you and financial freedom. The ages you can draw your state pension and personal savings are rising, salary-linked pensions have largely disappeared in the private sector, while unfavourable tax changes, tougher routes to home ownership and ongoing cost-of-living pressures are choking the ability to build and preserve wealth.

While this all sounds rather bleak, stopping work before old age is still within reach. The questions are: what are these key challenges? And how do you overcome them?

Early retirement, defined

Anyone who packs up work before state pension age, currently 66, technically retires early. But many strive to leave the labour force years before their mid-sixties, aspiring to life beyond employment at the earliest juncture.

The Financial Independence Retire Early (FIRE) movement is the most extreme example; a concept that’s seen growing adoption in recent years. Members of this group complement living frugally with saving and investing aggressively to accrue sufficient financial resource to down tools by their 30s or 40s.

Needless to say, the idea splits the crowd, but whatever your take on FIRE or any other strategy that aims to create total or partial financial freedom ahead of the majority, the long and short is that you get to design and define how your future looks.

No DB, no problem

The Financial Conduct Authority’s (FCA) Financial Lives survey 2025 found that as of May 2024, two in three adults (65%) who were receiving an income or had taken a cash lump sum from a pension had accessed a “gold-plated” defined benefit (DB) scheme.

This is important. DB arrangements provide the promise of a guaranteed income in retirement, calculated by your final or career average salary and number of years’ service, providing a ready-made replacement for lost earnings.

By contrast, only one in four (25%) current workers enjoy such schemes, and the vast majority of these will occupy public sector roles.

The workplace retirement shift from DB to defined contribution (DC), where you accrue a pot, the size of which is determined by what you pay in and how your investments perform, means current workers can ill-afford to neglect their retirement savings.

This has unequivocally made it harder to save for retirement as the risk has switched from employers to staff. Under auto enrolment, companies must contribute to employees’ pension, but the legal minimum is just 3% of “qualifying” earnings. In contrast, DB scheme contributions are typically north of 20%. DC savers need to pump in more in and are tasked with investing the money wisely. What’s more, if you opt for flexible income in retirement, you’ll need to continue managing your investments and making key decisions long after you leave the workforce.

All, however, is not lost.

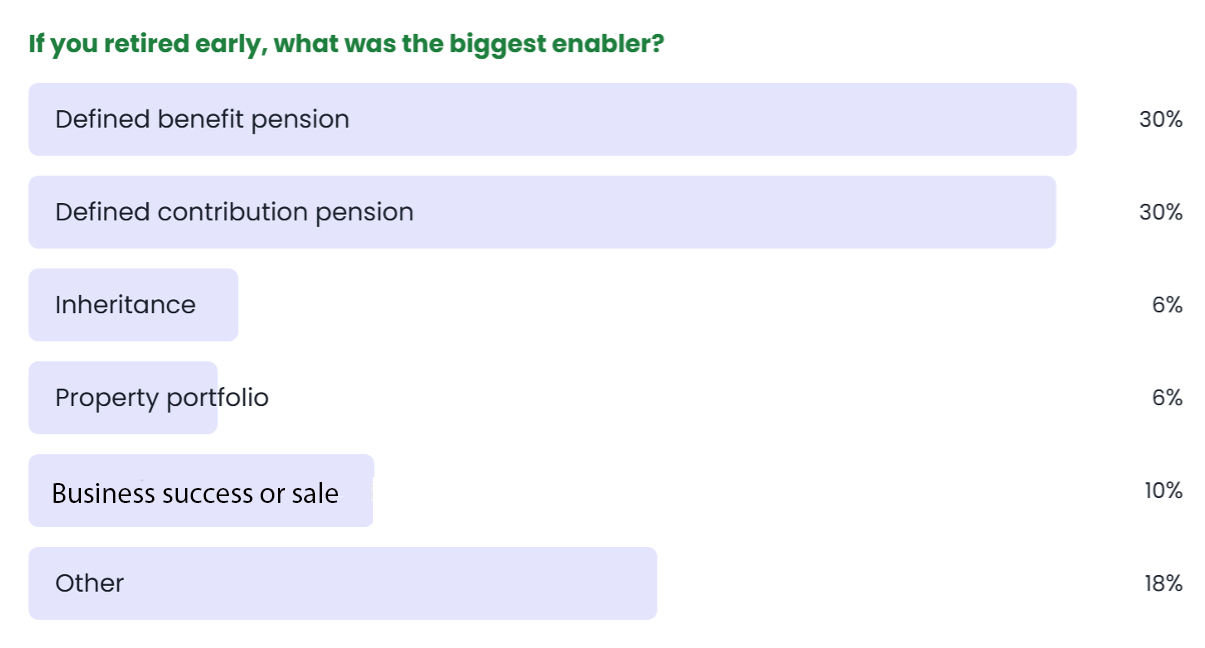

Last week I ran a poll on the ii Community app to learn more about the key products and strategies that enabled users to retire early. The results, garnering 560 votes, are shown below and paint a rather compelling picture.

As expected, DB pensions feature prominently, gathering 30% of the votes. But encouragingly, an equal percentage of DC schemes proved the main route to financial freedom, offering hope to those who missed the era of pension guarantees.

The fact that six in 10 named either DB or DC pensions as their biggest enabler, underscores just how valuable these retirement vehicles are. They’re not the only mechanism to grow wealth, but maximising employer contributions and upfront tax relief, especially if you pay higher rates of tax, are vital DC pension levers to pull if you want to save money quickly and easily. Plus, any growth escapes taxes, too.

Options to the poll centred purely on asset types, but the replies highlighted the grittier aspects required. One member asked me to add “Hard graft, investing and thriftiness” to the list of options, and this comment rang true with other users.

The message is: unless you receive a life-changing windfall, there’s no quick and easy route to early retirement, but it is doable.

Bridging the gap of pension age rises

An obstacle for those with DC pensions aspiring to retire in their early-to-mid-50s is the normal minimum pension age (NMPA) - the earliest point most pension pots can be accessed.

The direction of travel over the years hasn’t been favourable. Between 2006 and 2010, the NMPA stood at age 50 but is 55 today and will increase to 57 in 2028. Further rises, although not planned, are indeed possible. The longer you must wait to get your hands on your pension, the greater the burden on any accessible savings.

For those seeking to retire before the NMPA, stocks & shares individual savings accounts (ISA) are your friend. You may not enjoy relief on contributions, but withdrawals are tax free and you can access the cash whenever you please, creating a tidy bridge between stopping work and being able to draw from your DC pots.

- Is an ISA the missing part in your retirement plans?

- How to protect your pension from a midlife curveball

The rising state pension age may provide a further strain on personal resources. This increased from 65 to 66 in 2020, is in the process of hiking to 67, and scheduled to rise to 68 between 2044 and 2046. And with the third review of the state pension age under way, the timetable could be brought forward. Something else to mind here is that the earlier you leave the workforce, the less time you’ll have to accrue the necessary 35 years’ qualifying national insurance contributions (NIC) or credits to obtain the full state pension.

That doesn’t mean you should squash your dreams of stopping work early, but you may need some extra funds in pensions, ISAs or combination of the two to support your lifestyle in the interim.

Making the pot last

Retiring early is a steep mountain to climb, but perhaps the bigger challenge is to avoid tumbling back down. Assuming you live for an average number of years, your prospects are squeezed in several fronts: you have less time to put money away, reduced benefit from investing compounding, and assuming you live a long and healthy life, more time for your wealth to last.

Let’s crunch the numbers to work the savings pot for a 20-year-old, investing £500 every month with contributions ticking up 2% a year, achieving 5% annual returns after charges.

Age 45: £362,646

Age 55: £735,628

Age 65: £1,380,228

These figures are purely to illustrate the importance of time when building wealth. The amount you need to be financially independent could be more or less than this, depending on the lifestyle you aspire to.

But what the calculations show is that for every decade you bring retirement forward, your pot size halves. In addition, you have less time to build up the necessary deposit to buy a home, should that form part of your plan, and fewer years to pay off any loan.

Once you reach the level of wealth that you believe will provide financial freedom, the big task is developing a strategy to make the pot last. If you, say, stop working at age 50, your income strategy, should you wish to keep your pot invested and take income flexibly using drawdown, may need to span four (or perhaps five) decades.

Taking the natural yield may be the most appealing option, as it means you’re not depleting capital. However, yields can fluctuate, so there’s no guarantee the strategy will continue meeting your outgoings over time. Alternatives include taking a set withdrawal rate every year, the most common of these is the Bengen rule – which deems if you draw 4% a year from your portfolio, uprated annually to account for inflation, your pot should last at least 30 years. While the figure was recently updated to 4.7% and can act as a useful starting point and guide, the central drawback is that it’s not personalised and therefore might not be suitable for you.

- Is 4.7% the new magic number for sustainable pension withdrawals?

- Income from £250K, IHT and pensions, and are ETFs riskier than funds?

There are also major considerations when buying an annuity - a guaranteed income for life or a set period - in your 50s.

Namely, rates rise the older you are, as longevity plays a key role in what providers will offer you. To give you an idea, using current ballpark rates, a 55-year-old with a £500,000 pot buying an annuity that rises 3% a year, could expect to secure around £22,500 annual income, but this jumps to £29,600 for someone 10 years older.

Planning how to manage your wealth throughout retirement is key. You don’t have to buy an annuity immediately; you could adopt drawdown for a period then secure a guaranteed income once you reach a certain age when rates should be more attractive.

Know what you can control and what you can’t

Certain aspects of saving for retirement are within your control. These include how much you save, what this money is invested in, and the amount of tax you pay as your savings grow.

But others such as the future trajectories of stock markets, interest rates and inflation cannot be predicted with any accuracy. While further policy reform, favourable or not, is inevitable. The threats of these become more acute the longer your money must provide an income for. A few years’ red-hot inflation, like we endured earlier this decade, can cause lasting damage to your accrued savings, as it typically requires larger withdrawals to sustain your desired lifestyle.

- Tony Blair Institute’s radical proposal to overhaul state pension

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

The situation with house prices is a particularly high barrier to financial freedom. The average UK home costs around eight times the median salary, while the combination of frozen tax thresholds and a rising cost of living is restricting scope to build the necessary deposit. While home ownership isn’t essential to achieving early retirement, it can be a giant leap towards such a goal.

The need for personalisation and flexibility

One of the core themes here is the need to personalise your early retirement plan. A component of this is to build in flexibility to guard against the unexpected. Putting life’s curveballs to one side, you might fear how long your wealth will last or miss the routine and purpose of work.

Recent research by retirement house, Standard Life, found that 8% of retirees have already returned to the labour force and a further 8% are thinking about it. As you might imagine, financial pressures are a key factor but aren’t the only driver. Some are heading back to employment for non-financial reasons, such as to reconnect socially or tackle loneliness.

And this reminds us of something important. Financial freedom isn’t merely about stopping work; it’s about being able to live life on your own terms. For some, work is a fundamental aspect of what makes life enjoyable. You may wish to pursue jobs in old age that are more fulfilling but less lucrative, funding your outgoings through a mix of earnings and passive income.

Whatever your definition of early retirement, the labyrinth leading to this milestone isn’t getting any easier to navigate. Apparently, the solution to exit a maze is to walk continuously and keep one hand in constant contact with the wall. Transferring this logic to financial freedom: take regular and concentrated steps to boost your wealth, and always keep one eye on your financial plan.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.