Stockwatch: time to climb aboard this latest uptrend?

It’s been a volatile share, but the story appears to be developing well, and analyst Edmond Jackson expects a pattern of financial upgrades.

22nd May 2026 11:13

by Edmond Jackson from interactive investor

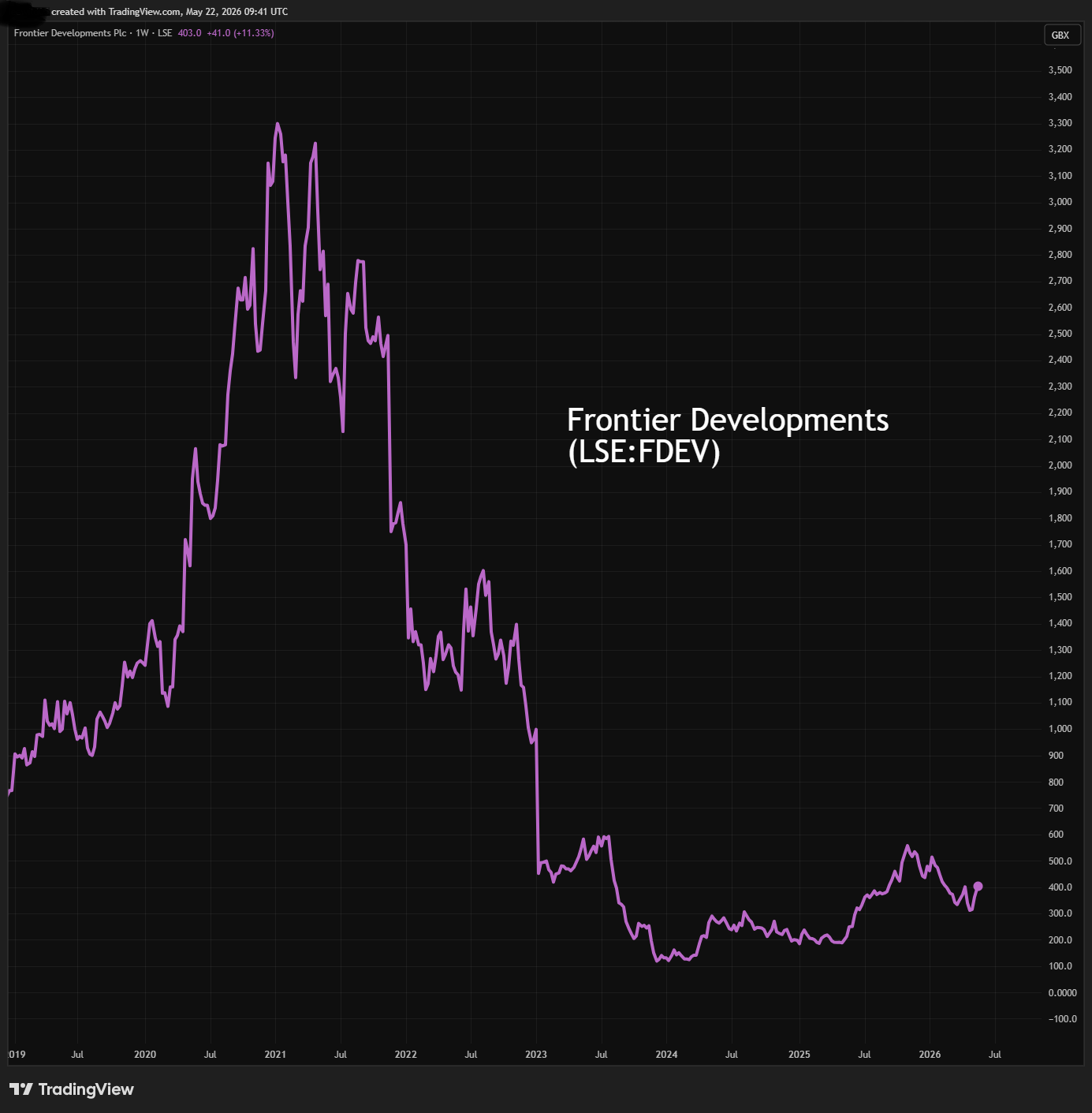

Is 400p a buying opportunity on the roller coaster of AIM-listed video games publisher Frontier Developments?

After the price soared from around 200p a year ago to 567p in November, it slumped from 529p in January despite punchy interim results and an upgrade to the full year to 31 May. It fell again to around 400p before the Iran war started, hitting a 302p low on 5 May.

- Invest with ii: Open a Stocks & Shares ISA | What is a Stocks & Shares ISA? | ISA Offers & Cashback

Just recently it rebounded, initially to about 400p after a 12 May update once again raised guidance in respect of the fiscal year closing, but then dipped and snapped back up to 400p, as if the technical situation has tested lows and buyers now prevail.

Source: TradingView. Past performance is not a guide to future performance.

Key value benchmarks are interesting

On the face of it, and assuming consensus for reported net profit just shy of £10 million, earnings per share (EPS) around 27p implies a price/earnings (PE) ratio near 15x, which can appear about right for a video games publisher of growth calibre albeit with volatile shares and no dividend.

Adjusting for £45 million end-April cash, however, a £142 million current market value is just 6x adjusted operating profit of around £16 million that is guided for, or 0.9x expected sales.

Frontier remains well down on highs above 3,000p achieved in early 2021, although that was on the back of euphoria around video games entertainment and share trading during Covid lockdowns. A market value above £1.1 billion was 10x sales of £114 million achieved in the fiscal year to 31 May 2022.

Perhaps the key question is whether it is justified to consider a mean-average valuation between “manic” four years ago and relatively “depressive” now – if considering also the business underwent a reset over the 2023 and 2024 fiscal years.

Tricky share to call but has attracted stake-building

I initially rated Frontier a “buy” at 245p in September 2024 after Viking Global Investors declared a 5% stake and management proclaimed, “the strongest-ever release of games to launch over three years”.

The shares did not rally until a 28 May 2025 update cited near flat annual revenue to 31 May of around £90 million, albeit ahead of expectations. An 11 June full-year update then said three games alone – Planet Coaster, Planet Zoo and Jurassic World Evolution – had generated 77% of total revenue versus 62% previously, cash was up 44% to £42.5 million, and a £10 million buyback was under way.

- City reacts to BT’s new dividend policy

- Trading Strategies: is BAE Systems overvalued after 270% rally?

- British Land’s ‘compelling fundamentals’ imply big upside

Last November I retained a “buy” stance at 560p after the £50-65 Jurassic World Evolution 3 was declared to have sold more than 500,000 units within the first two weeks of its 21 October launch, as if the company reset was generating sustainable profitability and growth.

Yet the shares fell from 529p after the 14 January interims showed a 26% revenue rise and 76% hike in adjusted operating profit on a 16.3% margin, plus a 47% jump in cash to £40.1 million. This was driven by highly positive player responses to Jurassic World Evolution 3 and Planet Zoo becoming Frontier’s highest grossing individual game by revenue, hence the foundation for a sequel.

Interestingly, Viking Capital appears to have used price weakness to raise its stake to 7.4% and JP Morgan has also built a 5.0% stake, last buying in April. There is also evidence of retail investors buying the drop.

As if reflecting underlying momentum, last December showed that month’s second-highest revenue in the vital Christmas trading period, and full-year guidance to 31 May was upgraded both for revenue and profit.

The interim statement did show a 6.5% rise in R&D expenses to near £17.4 million – the key cost for games developers – yet can be seen as potentially positive for sales.

Meanwhile, sales and marketing costs eased 3% to £4.9 million but administrative expenses rose 18% to £8.3 million. Pre-tax profit still jumped 82% to almost £8.0 million.

That no adverse news was declared as the shares fell, and with an £8 million share buyback programme launched on 26 February and due to complete by 27 June, shows how buybacks do not necessarily support share prices.

From 2 March, Frontier’s founder and president did engage another pattern of share selling which continued to 22 April (repeating sales from July to September), although he remains by far the largest shareholder at 32.6%.

Frontier Developments - financial summary

year end 31 May

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| Turnover (£ million) | 21.4 | 37.4 | 34.2 | 89.7 | 76.1 | 90.7 | 114 | 105 | 89.3 | 90.6 |

| Operating margin (%) | 5.8 | 20.9 | 8.2 | 21.6 | 21.8 | 22.0 | 1.4 | -25.4 | -31.8 | 14.0 |

| Operating profit (£m) | 1.2 | 7.8 | 2.8 | 19.4 | 16.6 | 19.9 | 1.5 | -26.6 | -28.4 | 12.7 |

| Net profit (£m) | 1.4 | 7.7 | 3.6 | 18.0 | 15.9 | 21.6 | 9.6 | -20.9 | -21.5 | 16.4 |

| Reported EPS (p) | 4.1 | 22.4 | 9.1 | 44.7 | 39.4 | 53.3 | 23.7 | -53.6 | -55.6 | 40.7 |

| Normalised EPS (p) | 4.1 | 22.4 | 9.1 | 44.7 | 39.4 | 53.3 | 35.6 | -23.4 | -24.7 | 40.7 |

| Return on total capital (%) | 5.1 | 23.5 | 5.0 | 25.6 | 13.0 | 13.9 | 1.1 | -22.4 | -28.4 | 10.9 |

| Operating cashflow/share (p) | -3.6 | 13.5 | 25.9 | 81.5 | 80.4 | 96.3 | 101 | 123 | 81.9 | 103 |

| Capex/share (p) | 1.0 | 2.3 | 46.0 | 42.9 | 53.8 | 81.2 | 95.4 | 111 | 78.7 | 76.3 |

| Free cashflow/share (p) | -4.6 | 11.2 | -20.1 | 38.6 | 26.6 | 15.1 | 5.6 | 12.0 | 3.2 | 26.8 |

| Cash (£m) | 8.6 | 12.6 | 24.1 | 35.3 | 45.8 | 42.4 | 38.7 | 28.3 | 29.5 | 42.5 |

| Net debt (£m) | -8.6 | -12.6 | -24.1 | -35.3 | -22.2 | -20.3 | -18.0 | -9.0 | -8.2 | -23.0 |

| Net assets (£m) | 22.8 | 31.3 | 55.3 | 74.2 | 96.7 | 113 | 118 | 96.0 | 76.8 | 95.2 |

| Net assets/share (p) | 66.8 | 91.4 | 143 | 192 | 249 | 288 | 300 | 243 | 195 | 241 |

Source: historic company REFS and company accounts.

A twist regarding future content releases

The update on 12 May was overall bullish in terms of raising annual revenue guidance by 3% to around £103 million amid ongoing success of Jurassic World Evolution 3 combined with strong ongoing sales across Frontier’s other games.

Adjusted operating profit was guided up 45% to £16 million albeit significantly due to higher-than-expected tax credits following a transition from the Video Games Tax Relief regime to Video Games Expenditure Credits. Revenue has been stronger than expected too.

Year-on-year cash has risen from £42.5 million to £44.9 million despite £15.4 million of buybacks over the period that should enhance EPS by 11% in the May 2027 year and beyond. The operating cash inflow would otherwise have been £17.8 million.

There was also a twist, with the company stating: “Cumulative revenue for JWE 3 is ahead of JWE 2 like-for-like although in the last month delays beyond Frontier’s control have impacted the release of further content for the game. Frontier is working hard to resolve these matters and return to its planned content roadmap.”

- How to make early retirement a possibility

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Tax burden on pensioners surges: how to cut your bill

From what I can see online, there is speculation that Universal Studios, the intellectual property owner, has changed its scheduling of future Jurassic World films, given that the next movie was expected to be declared at an industry convention in April but was not. There has been silence across all four main Jurassic World social media accounts from last March. Requiring Universal’s approval thus pushes forward when Frontier can develop and release related content.

That Jurassic World Rebirth released on 2 July last year has grossed $886 million (£665 million), and it would seem likely that Universal will want to sustain momentum, so any delay to Frontier should not compromise forecasts.

An attractive medium-term ‘buy’

The underlying story sounds like it is developing well at Frontier and should result in a pattern of financial upgrades, notwithstanding occasional disruption like appears the case now. Despite a challenged outlook for discretionary consumer spending, if video games hit the spot with followers, then a publisher can easily buck the general trend.

Larger studios are prone to acquire smaller ones, hence there is possible long-term takeover interest, although Frontier has been listed since 2013.

The share’s 50-day moving average is now gently moving up, so unless there is no resolution to the US/Iran war such that oil prices move significantly higher this summer, prompting another wave of “risk-off”, I think retaining a “buy” stance on Frontier is appropriate.

A post year-end trading update is due on Wednesday 10 June.

Edmond Jackson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.