American pioneers: investment trusts with less tech

Kepler examines trusts that could be a good match for those seeking to diversify their US exposure beyond Big Tech.

15th May 2026 14:07

This content is provided by Kepler Trust Intelligence, an investment trust focused website for private and professional investors. Kepler Trust Intelligence is a third-party supplier and not part of interactive investor. It is provided for information only and does not constitute a personal recommendation.

Material produced by Kepler Trust Intelligence should be considered a marketing communication, and is not independent research.

Lucky Luke, the main character of the eponymous comic series, is best known for his shooting skills, earning him the epithet ‘the man who shoots faster than his shadow’. This ability enables him to emerge unscathed from numerous face-offs with the criminals populating the American Wild West and to triumphantly ride back home at the end of each episode.

Beyond the geographical setting, this may bear some resemblance to US equities. For example, their long-term track record of outperforming the rest of the world could be reminiscent of Lucky Luke’s invincibility, while their ability to grow earnings faster than their global peers could be likened to the gunslinger’s shooting prowess.

Since late 2022, following the initial launch of ChatGPT by OpenAI, earnings growth in the US has been driven largely by companies linked to artificial intelligence (AI), with the market strongly rewarding these stocks. However, the AI rally has been highly concentrated in a handful of names, notably chip designers and hyperscalers, which now dominate US equity indices.

Using the MSCI USA Growth Index as a proxy for tech mega-caps, we note that these companies are expected to continue delivering significantly higher earnings growth than the broader US equity market as well as the rest of the world over the next one to two years, albeit at elevated valuations.

However, in recent months, trust managers have been dialling down their exposure to the tech mega-caps and the companies that have led the AI trade. But while this industry has become almost synonymous with the US equity market, it is not simply a case of selling America, as we discuss below.

VALUATION AND EARNINGS GROWTH EXPECTATIONS

| Measure | MSCI USA Growth | MSCI USA | MSCI ACWI ex USA |

| P/E (forward to the end of 2027) (x) | 24.7 | 19.3 | 13 |

| P/E (forward to the end of 2028) (x) | 20.8 | 17.2 | 11.9 |

| Earnings growth (1-yr forward) (%) | 21.7 | 13.4 | 13.1 |

| Earnings growth (2-yrs forward) (%) | 17.4 | 11.4 | 9 |

Source: Bloomberg, as at 06/05/2026.

Riding out of tech mega-caps

Since late 2024, several managers of global equity trusts have reduced their exposure to AI-related mega caps. In addition to elevated valuations, they have cited concerns about the substantial capital expenditures being undertaken by these companies and whether they will ultimately generate adequate returns.

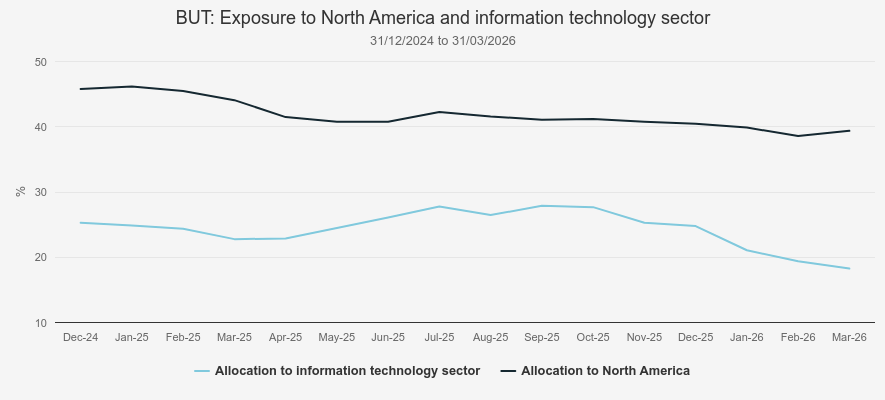

For example, the managers of Brunner Ord highlight the relatively low monetisation of AI products until now. As a result, they reduced their allocation to semiconductor companies in 2025. That said, they remain cognisant of AI’s disruptive potential and have exited positions in companies whose business models they believe could be at risk. As such, BUT’s exposure to the information technology sector and the North American region has decreased significantly since the start of 2025, as the chart below shows. Instead, they have allocated to companies embedded in the physical world, including US-listed businesses, where they see a lower risk of disruption. One example of such stocks is Federal Signal Corp, an Illinois-based manufacturer of specialised vehicles such as street sweepers and road-marking lorries.

SECTOR AND GEOGRAPHICAL EXPOSURE

Source: Allianz Global Investors.

Similarly, the managers of Invesco Global Equity Income Trust ord, Stephen Anness and Joe Dowling, have trimmed their allocation to semiconductor companies and recycled the proceeds into unloved parts of the market. That includes the US healthcare sector, where Stephen and Joe initiated two new positions in December 2025 alone. We note that healthcare companies have faced headwinds under the current US administration, particularly due to uncertainty caused by trade tariffs and pressures on pharmaceutical companies to reduce drug prices.

However, taking a longer-term view, we believe the sector offers exposure to structural growth themes, including ageing populations and continued innovation in drugs and medical devices. In addition, the defensive and non-cyclical nature of many healthcare companies may provide resilience in the event of an economic slowdown. Stephen and Joe have also found attractive opportunities in the US financials sector, including East West Bancorp Inc, which primarily serves Chinese American customers. They see it as one of the best banks they have ever analysed, viewing its CEO as an exceptional steward of capital and highlighting the company’s underwriting performance during the global financial crisis.

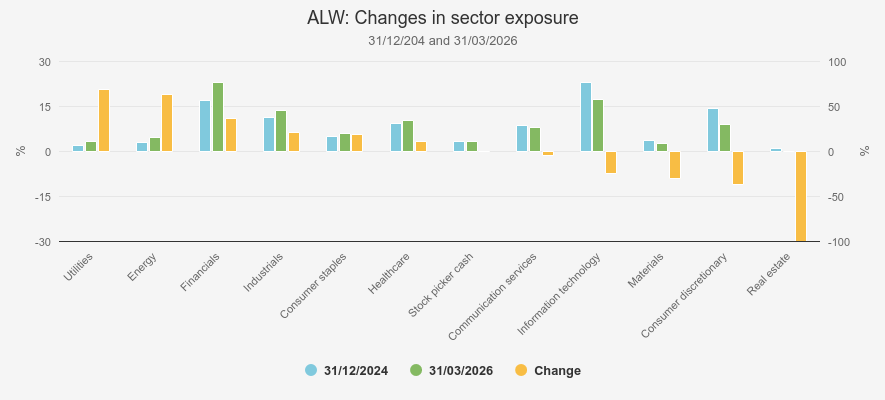

Some of the stock pickers within the multi-manager strategy Alliance Witan Ordhave also trimmed their exposure to US tech mega caps since late 2024, reducing the trust’s allocation to North America and the information technology sector, as the bar chart below shows. These stock pickers note that free-cash-flow generation at many of these companies is being squeezed by elevated capital expenditure. Instead, they have reallocated towards businesses in more defensive sectors such as healthcare, consumer staples, and utilities, as well as in the energy sector, highlighting that these companies offer more attractive valuations alongside reliably growing free cash flow.

GEOGRAPHICAL EXPOSURE

Source: Willis Towers Watson.

Meanwhile, the team at Marylebone Partners, which has managed Majedie Investments Ord since 2023, continues to have very limited exposure to US tech mega-caps. They have long held the view that there are opportunities in the US offering superior risk-adjusted returns outside of these names. This includes, among others, mid-cap biotechnology firms and undervalued software companies, which they access through specialist third-party funds. Since the start of the year, they have taken advantage of the sell-off in software businesses, triggered by fears of AI disruption, to increase their exposure. They believe the sell-off has been overdone and that many software companies benefit from strong competitive advantages and are deeply embedded in their users’ operations, making them difficult to displace.

Conversely, Paul Niven, manager of the multi-manager strategy F&C Investment Trust Ord, remains constructive on AI-related mega caps. In his view, their premium valuations may not be excessive over a ten-year horizon, given their ability to deliver superior earnings growth, and he believes the market may be approaching a phase of broader AI adoption. That said, as Paul has trimmed exposure to one of the trust’s global funds, which is primarily exposed to US equities, to fund share buybacks, FCIT’s exposure to both the US and the information technology sector has slightly reduced too.

On the trail of overlooked opportunities

While the US equity market has become increasingly associated with tech mega caps, we think it is worth remembering that it is a broad market, home to many leading companies across a range of industries. Many of these have been overlooked amid the AI rally, despite offering exposure to other structural growth themes or benefitting from operational improvements. In fact, some of the constituents of the AIC North America sector have been increasing their exposure to these areas.

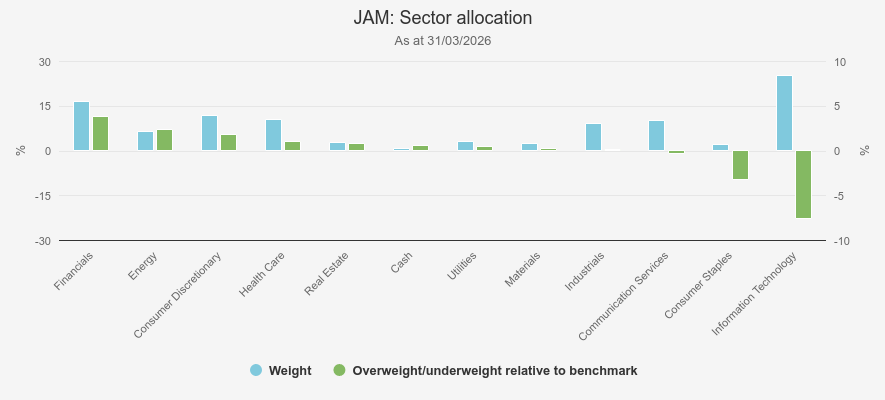

This is notably the case forJPMorgan American Ord. Like the managers of IGET, they have identified several opportunities in healthcare. They observe that, with the exception of companies involved in GLP-1 therapies such as Eli Lilly and Co, the sector has been largely ignored since the post-Covid reopening. For example, they built a new position in multinational pharmaceutical company Johnson & Johnson, which was trading at a discount to peers at the time of purchase, while exhibiting stronger profitability metrics.

The JAM management team has also increased exposure to the so-called ‘have-nots’ in the industrials sector, referring to the constituents that have not benefited from the AI-driven infrastructure build-out. The managers believe these companies are trading at attractive valuations, while also beginning to show signs of operational improvement in some cases. This includes 3M Company, which produces industrial and consumer goods and was added to the portfolio over the past year, with the managers highlighting that the business is now beginning to deliver organic growth. Finally, they have also initiated new positions in energy companies, highlighting that some businesses within the sector have the potential to grow independently of price movements in the underlying commodities they sell (e.g. oil). This includes, for instance, Exxon Mobil Corp, which is expanding into new areas such as low-carbon solutions.

SECTOR ALLOCATION

Source: JPMorgan.

Meanwhile, the managers ofNorth American Income Trust Ord, Fran Radano and Jeremiah Buckley, find quality companies attractive at this juncture. Last year was particularly challenging for those stocks, as the markets favoured more speculative, often pre-profit or loss-making names. As such, Fran and Jeremiah took advantage of these headwinds to build new positions. In terms of sector allocation, they remain overweight in healthcare and financials, as they believe companies in these sectors could benefit from a more balanced regulatory environment in the US. They have also moved from an overweight to a neutral position in information technology over the trust’s previous financial year. However, we note that the trust has had limited exposure to tech mega caps, as these typically pay low or no dividends and are, therefore, difficult to reconcile with NAIT’s income mandate.

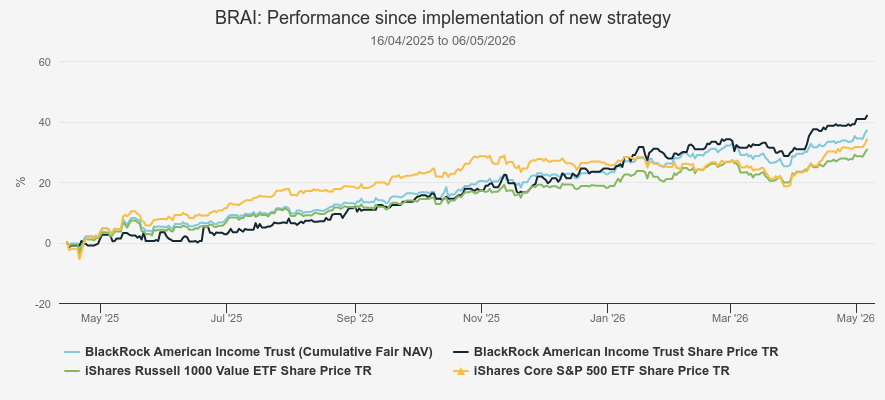

Travis Cooke and Muzo Kayacan, who have managed BlackRock American Income Trust Ordsince April 2025, also find quality companies compelling at this juncture, highlighting that companies with strong fundamentals have historically outperformed over the long term. That said, they continue to see short-term opportunities in AI-related stocks. Interestingly, despite BRAI’s emphasis on the value factor, the trust holds names such as Alphabet Inc Class A and Amazon.com Inc. This is because stock inclusion in its benchmark, the Russell 1000 Value, is determined by valuation metrics such as lower price-to-book ratios, meaning that relatively cheaper tech mega caps have entered the index and, by extension, BRAI’s investment universe. We also note that Travis and Muzo have made a strong start as managers of BRAI, having outperformed both their benchmark and the S&P 500 index since their appointment, as the chart below shows.

PERFORMANCE UNDER CURRENT STRATEGY

Source: Morningstar. Past performance is not a reliable indicator of future results

Beyond the mega caps, the US is also home to many lesser-known businesses plugged into the AI theme across both public and private markets. In fact, Baillie Gifford US Growth Ordhas initiated new positions in some of these over its previous financial year. This includes Runway, a generative AI video platform, with managers Gary Robinson and Kirsty Gibson viewing the unlisted business as a pioneer in the use of machine learning in creative workflows. They also built a position in Globant SA, a listed IT services provider, which they expect to benefit from companies seeking support to integrate AI into their operations.

That said, USA offers exposure to more than just AI, and some of the recent additions to the portfolio are unrelated to this theme. This includes, for example, SharkNinja Inc, which they see as gaining market share in the home appliance market, and online sports betting company DraftKings Inc Ordinary Shares - Class A, which they believe will benefit from looser regulatory barriers. However, we note that Saba Capital still holds a c. 29% stake in the trust and has previously attempted to replace the trust’s board with its own nominees, as well as blocking a merger with Edinburgh Worldwide Ord. As such, we believe further activism by Saba cannot be ruled out.

Conclusion

We find it interesting that healthcare has been a common destination for a number of investment trust managers seeking to diversify away from tech mega caps. As discussed, it is a sector that has faced several headwinds, notably since the last US election, but it continues to offer exposure to long-term structural growth themes. In addition, it comprises companies with both offensive and defensive characteristics. As such, we think the healthcare sector could thrive in both a buoyant market environment and during an economic slowdown.

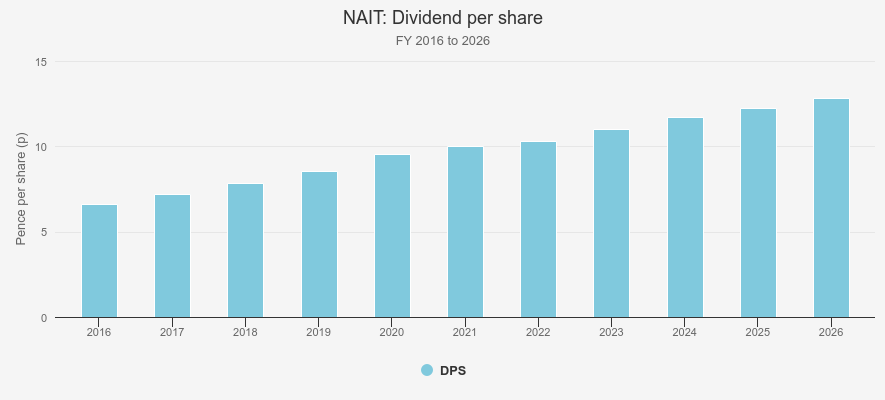

NAIT has a particularly high allocation to this sector, at 16.5%. This represents a 610 basis point overweight relative to its benchmark, the Russell 1000 Value Index. As such, the trust could provide an attractive way to gain exposure to the healthcare sector. In addition, NAIT could offer diversification within a US allocation, given that its income mandate naturally steers the portfolio away from tech mega caps, as these stocks tend to pay low or no dividends, resulting in a differentiated exposure compared with a core US equity strategy. Moreover, we note that NAIT is the only US equity-focused constituent of the AIC North America sector to have a long-term track record of annual dividend increases, spanning 15 years.

DIVIDEND PER SHARE

Source: Janus Henderson. Past performance is not a reliable indicator of future results

We also find JAM’s positioning interesting at this juncture. The trust has added to its exposure to areas that have been overlooked amid the AI rally, including healthcare, while also maintaining exposure to tech mega caps. As such, we think the trust should be able to capture upside across different scenarios, including a continuation of the AI rally or a broadening of market returns.

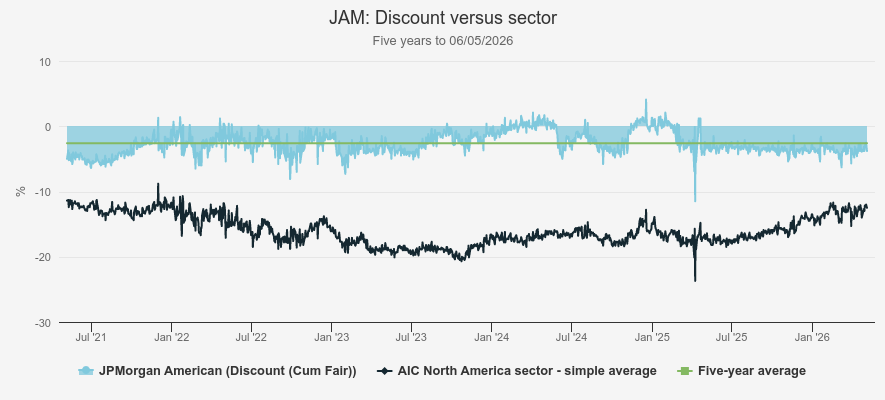

At the time of writing, JAM was trading at a 3.8% discount. Albeit modest, this was also the widest discount among US equity-focussed investment trusts in the AIC North America sector (with the exception of Pershing Square Holdings Ord). This was also slightly wider than the trust’s long-term average, with the trust having consistently traded at narrow discounts or premiums. In fact, JAM still commanded a small premium until early 2025. We think the loss of this premium reflects the weaker relative performance the trust delivered last year, with the market favouring more speculative names, whereas JAM focusses on high-quality companies. However, this could reverse if the recent changes in the portfolio prove successful.

DISCOUNT

Source: Morningstar.

Overall, we think the US continues to offer many exciting opportunities for growth, and the AI craze may have left some opportunities on the table to get access at a good price. While there is a lot of talk of rotating away from the US, we think it’s important not to throw the baby out with the bathwater.

Kepler Partners is a third-party supplier and not part of interactive investor. Neither Kepler Partners or interactive investor will be responsible for any losses that may be incurred as a result of a trading idea.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Important Information

Kepler Partners is not authorised to make recommendations to Retail Clients. This report is based on factual information only, and is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

This report has been issued by Kepler Partners LLP solely for information purposes only and the views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment. If you are unclear about any of the information on this website or its suitability for you, please contact your financial or tax adviser, or an independent financial or tax adviser before making any investment or financial decisions.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. Persons who access this information are required to inform themselves and to comply with any such restrictions. In particular, this website is exclusively for non-US Persons. The information in this website is not for distribution to and does not constitute an offer to sell or the solicitation of any offer to buy any securities in the United States of America to or for the benefit of US Persons.

This is a marketing document, should be considered non-independent research and is subject to the rules in COBS 12.3 relating to such research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research.

No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not to be taken as advice to take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm's internal rules. A copy of the firm's conflict of interest policy is available on request.

Past performance is not necessarily a guide to the future. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice should be taken before entering into any financial transaction.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is a limited liability partnership registered in England and Wales at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority.