The 11 ‘forever shares’ I’ve picked for my kids’ Junior ISAs

At the beginning of the new tax year, analyst John Ficenec reveals where he’s investing his children’s ISAs, how he’s achieving adequate diversification and why timing is irrelevant.

15th April 2026 10:11

by John Ficenec from interactive investor

Turmoil in financial markets caused by uncertainty over the direction of the Iran war could cause investors to be wary of looking at shares right now.

However, when it comes to setting up an ISA portfolio for my children, I’m much more sanguine about putting some cash to work. So, here is my list of crash-proof shares to tuck away and secure the next generation’s financial future.

- Invest with ii: Open a Junior ISA | ISAs for Grandchildren | Junior ISA Allowance

Looking through the price anchor

The key issue to start with is that the share price now matters very little to the returns of the portfolio in the long run. The most important element is to get started putting that cash to work. Behavioural science has shown that once you’ve begun, much like subscription models, most of us will stick with it. The biggest risk is that we delay decisions because the shares look too expensive when trading is good, or too risky when they are cheap and trading is bad. Once delayed, the investment is promptly forgotten.

To best demonstrate this, I’ll use Shell (LSE:SHEL) shares as an example. The average price for Shell during the past two decades has been around £21. Shell also pays out healthy dividends, amounting to £22.90 ($30.93) per share during the past 20 years. Then there is the performance of the shares which have now gained around 62% from our average £21 purchase price to around £34.

If I’d bought the shares 20 years ago and made regular investments, I’d have received a hefty income, share price gains and benefited from compounding returns from reinvestment of dividends. It would be impressive over a shorter 10-year period, too.

It’s easy to forget that the past 20 years have not been easy for Shell. Oil prices collapsed in 2015 and 2020, and twice the shares have sunk below £15 as profits tumbled. The dividend was also cut by 65% in 2020. The reason I would be happy to put Shell shares in my children’s portfolio is exactly because of these troubles; it has proven to be a survivor. When looking for shares for the portfolio, it is longevity and staying power I’m after.

- How fund pros invest in Junior ISAs for children or grandchildren

- Junior ISAs (JISA): all you need to know

The share price may be at an all-time high, but as I’ve shown, that isn’t important. It doesn’t “lock-in” a high price from which the investor never recovers, rather it is an indication of the value the market has attached to the potential income generation.

The other key assumption when building this portfolio is that I know nothing about what will happen in the future. That means strong balance sheets and some steady dividend income are all important parts of the decision-making process.

Diversification, diversification, diversification

To spread the risk, there needs to be diversification across the different equity sectors. Once again, to keep it simple, I’m just picking one share for each of these sectors - Information Technology, Financials, Healthcare, Energy, Consumer Discretionary, Consumer Staples, Communication Services, Industrials, Materials, Utilities, and Real Estate.

Starting with Information Technology, again I’m looking for longevity and dividends so, despite the recent sell-off, I’m happy to go with Microsoft Corp (NASDAQ:MSFT). Among financials, insurance has offered some steady returns, so Prudential (LSE:PRU) fits the bill for me. For healthcare, and despite a record run, I like AstraZeneca (LSE:AZN)’s strong pipeline of new medicines.

Shell is my Energy pick and Games Workshop Group (LSE:GAW)’s excellent track record makes it my choice in Consumer Discretionary. The recent troubles at Unilever (LSE:ULVR), with the food spinoff to McCormick and exit of the ice cream business earlier this year, should hopefully leave a more focused Consumer Staples company.

BT Group (LSE:BT.A), in Communication Services, has not had a great past two decades, with the shares almost exactly where they were in 2006, but then again this is about staying power, not just flash-in-the-pan companies, so in they go.

For an Industrial share, it’s trickier as BAE Systems (LSE:BA.) shares are also at an all-time high, but, as I’ve already showed, it doesn’t really matter in the long run. What I want is bullet-proof shares, so in they go.

For Materials, I think most miners are much of a muchness, but with slightly different focuses on base metals. However, of the iron ore giants, Rio Tinto Ordinary Shares (LSE:RIO) is solid. Utilities have been getting press for all the wrong reasons when it comes to water, so I’ll go for the electricity network provider National Grid (LSE:NG.). And finally, for Real Estate, there are some attractive dividends as the sector has sold off as interest rates have risen, so British Land Co (LSE:BLND) should fit the bill.

Sector | Company name |

Information Technology | Microsoft |

Financials | Prudential |

Healthcare | AstraZeneca |

Energy | Shell |

Consumer Discretionary | Games Workshop |

Consumer Staples | Unilever |

Communication Services | BT |

Industrial | BAE Systems |

Materials | Rio Tinto |

Utilities | National Grid |

Real Estate | British Land |

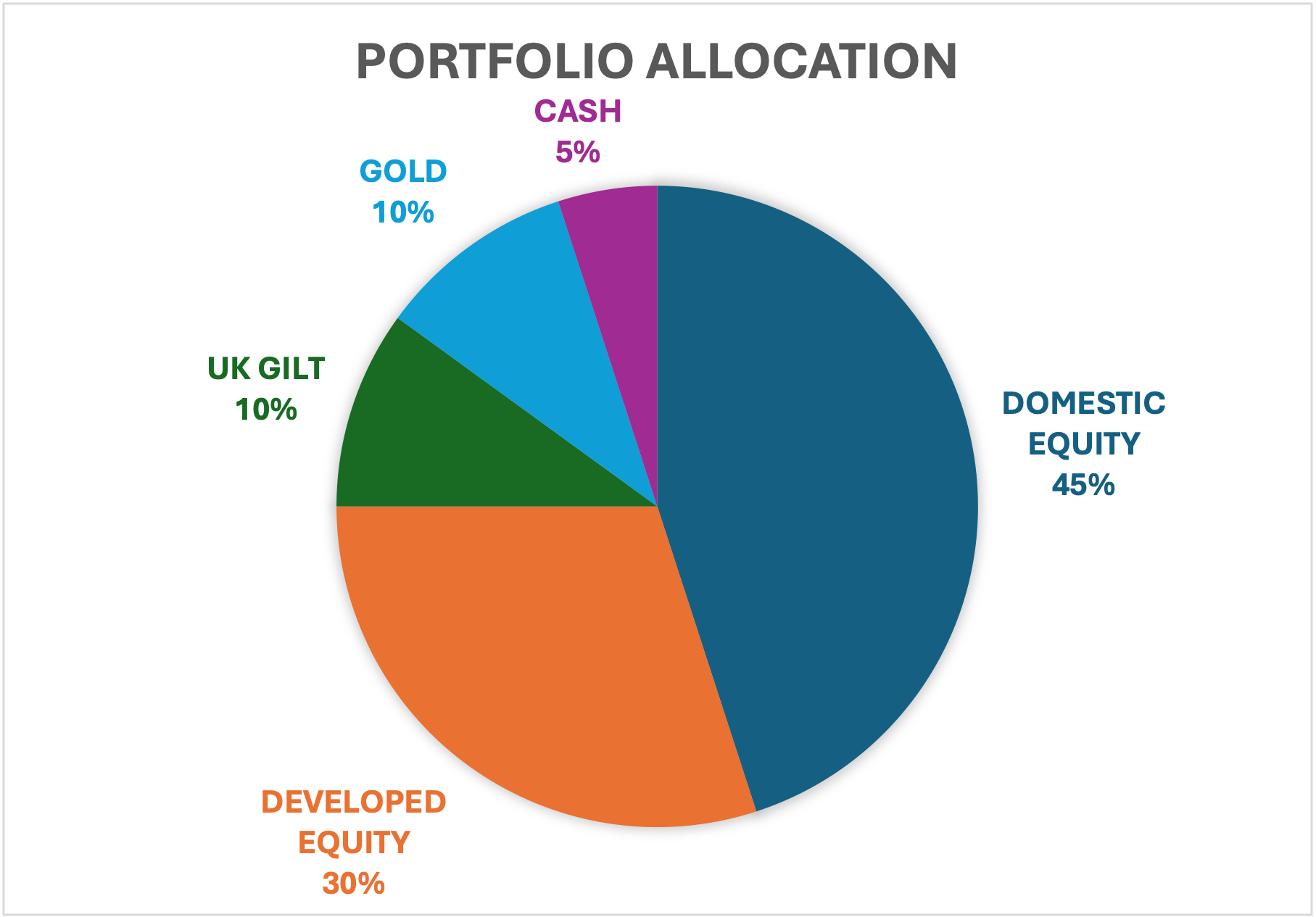

Asset classes

As well as spreading risk across sectors, it is just as important to make sure not everything is held in shares. So, I’m choosing a commodity like gold to protect against currency devaluation and inflation over time. A gold-focused exchange-traded fund (ETF) such as iShares Physical Gold ETC GBP (LSE:SGLN) helps spread risk. Also, some fixed income in the form of UK gilts (LON:T46) that mature in 20 years and offer a coupon of 4.25% are worth considering for diversification.

Portfolio allocations are always just a guide as they can prove tricky for retail investors to stick to religiously. For example, a company such as Shell might be nominally a UK-listed share, but it generates all its earnings in US dollars from around the world and, as such, really should be considered a developed world equity not a domestic equity for risk purposes.

- Are you maximising your family’s ISA allowances?

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

With that in mind, I always use the asset allocation as a sense-check to make sure I haven’t missed anything rather than a cast-iron rule for what should be in there at any one time.

Slow and steady wins the race

A good range of assets and shares across different sectors greatly de-stresses the investment process. It then becomes more a focus on regularly targeting a cash amount to put into the portfolio each year. As and when that cash amount is put into the portfolio, the decision is often made for you already depending on which sector or weighting is slightly light. This will often happen if the cash amount is a regular small instalment as it won’t always be possible to allocate evenly each time. For example, Astra Zeneca shares are currently around £150 each, Rio Tinto £73, while BT are £2.18.

The most important element with longer-term investments like these, especially when the recipients have a horizon well in excess of 40 years, is simply to get started as soon as possible. It is too easy to find an excuse or a concern to not invest in the first place, and that is a bigger risk than beginning to invest. Remember, time and compounding are the great allies of the investment portfolio.

John Ficenec is a freelance contributor and not a direct employee of interactive investor.

Important information: Please remember, investment values can go up or down and you could get back less than you invest. If you’re in any doubt about the suitability of a Stocks & Shares ISA, you should seek independent financial advice. The tax treatment of this product depends on your individual circumstances and may change in future. If you are uncertain about the tax treatment of the product you should contact HMRC or seek independent tax advice.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.