What would a longer war in the Middle East mean for investors?

Financial markets are currently only pricing in a short conflict in Iran, but the longevity and outcomes of warfare are often unpredictable. Analyst John Ficenec looks at different scenarios.

10th March 2026 10:58

by John Ficenec from interactive investor

Markets are currently pricing in a quick resolution to the conflict in Iran, and this has important implications for investors seeking to protect their savings and deliver positive returns in the year ahead.

- Learn with ii: ISA Allowance | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Commodity markets bet on short war

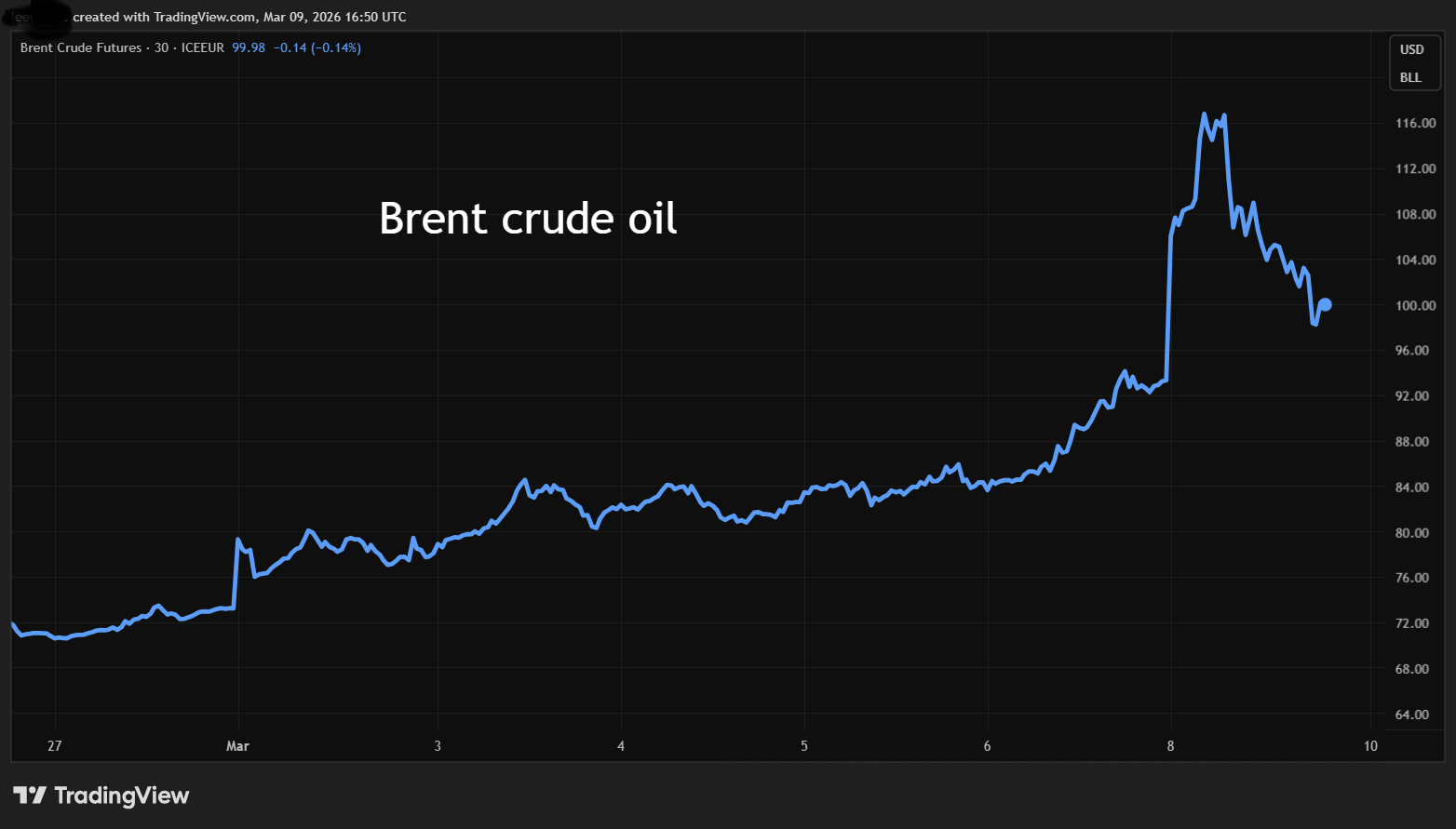

All the headlines are focusing on a spike in the oil price, but a lesser reported number which predicts the future price of oil could be more useful for investors. Most press reporting focuses on the spot price of Brent crude oil. This is the price of one barrel of oil in dollars, produced from the North Sea, that is then used as a global benchmark to price oil commodity contracts around the world.

It is called a spot price because it is made up “on the spot” by trading desks in banks and commodity trading houses, based on supply and demand. This spot price is also for the immediate purchase of one barrel of Brent light sweet crude, with payment now and delivery on the same day. As such, even though Brent crude is produced in the North Sea, over 4,000 miles from Iran, it still reflects how the crisis there has impacted the global market for oil.

The spot price for oil today reflects that the Strait of Hormuz, through which about 20% of the world’s oil supply travels, is currently closed, and the Middle East, which produces about 30% of the world’s oil and closer to 50% of oil exports, is under threat. So, Brent crude shot up to almost $120 a barrel from $60 at the start of the year.

Source: TradingView. Past performance is not a guide to future performance.

Henry Allen, macro strategist at Deutsche Bank, has pointed out that the price for the same barrel of Brent crude oil, but for delivery a year in the future, has only increased to around $70. The almost $30 difference against today’s price is because commodity markets are betting this is a short-term conflict. Despite the damage to oil infrastructure, the futures price is predicting that oil production can return to normal within two months, and that a largely normal trade of oil and gas will resume through the Middle East.

Markets sigh not sink

That is why stock markets have only sold off slightly from record highs and not collapsed. The UK blue-chip FTSE 100 index has slipped as much as 6% lower since 27 February but is still up for the year. The drop is comparable to early November last year when the FTSE 100 fell 4.5% on Autumn Budget and growth fears. You’d expect a far greater fall if the current events in Iran resulted in oil and gas prices staying at these levels.

- Ian Cowie: an investment trust to hold in febrile times

- Where investment professionals are investing their ISA

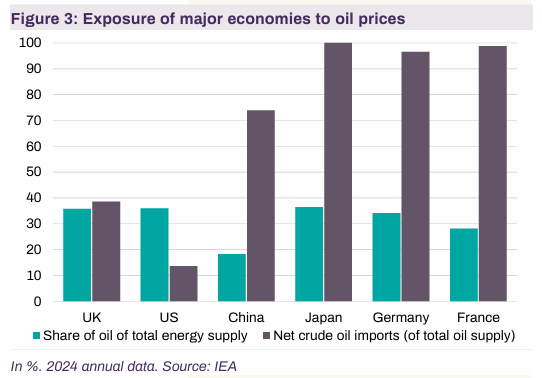

In the US, the S&P 500 index is only down 2.5% since 27 February and is now down 2% so far in 2026. This to some extent reflects that America with its own oil and gas production is insulated from a price spike. The same cannot be said for Asia where South Korea, China and Japan are more reliant on oil imports, which explains why stock markets in these regions are down 16%, 2% and 10% respectively.

What could trigger a sell-off?

Deutsche Bank’s Allen added that one of three conditions must usually be met to cause a larger sell-off, such as a 15% drop in the US S&P 500 in equity markets. The first is that oil and gas prices need to remain elevated for several months. The second would be that this results in a government response to combat inflation such as raising interest rates or slowing money supply. The third would be that the shock is enough to result in a meaningful economic slowdown. While the attacks across the Middle East move us closer to each of those requirements, none are currently met.

The best way to look at this is how investors can respond to each of the outcomes. Depending on the risk appetite of each investor, you can then make a more informed decision.

Scenario 1: short-term conflict, stagflation avoided

If the commodity markets are correct and the conflict is short term, with Trump declaring victory by his own defined terms, then the inflationary shock will be mild. Kallum Pickering, chief economist at broker Peel Hunt, thinks that despite significant disruption across all major economies, the likely impact will be modestly higher inflation from the summer onwards, which begins to fade by the end of the year.

This is against a backdrop of falling inflation. In the UK, the consumer price index (CPI) finished last year at 3.6%, and Pickering expects it to drop to 2.5% by the end of this year, but 0.3% higher than the 2.2% forecast before the war started.

The response to a slight increase in inflation is that central banks wouldn’t really change the direction of travel on policy, just tweak the timing. So, in the UK where the Bank of England had been expected to cut this month, they could delay the decision to later in the year. In the US, the Federal Reserve could also move their expected interest rate cuts to later in 2026.

Recent opinion polls have shown the war is unpopular in the US, and investors have come to rely on the so-called TACO trade as Trump Always Chickens Out. In this scenario, investors can take advantage of bargains as markets have oversold UK shares in sectors such as mining, holiday and leisure, energy reliant industrials, or those industrials exposed to the aviation industry.

Source: TradingView. Past performance is not a guide to future performance.

Industrials that are heavy energy users such as engineer Rolls-Royce Holdings (LSE:RR.), Melrose Industries (LSE:MRO) and Weir Group (LSE:WEIR) would typically bounce back. Miners like Anglo American (LSE:AAL), Rio Tinto Ordinary Shares (LSE:RIO) and Antofagasta (LSE:ANTO) are also now cheaper on fears about growth in Asia. Holiday groups easyJet (LSE:EZJ), Jet2 Ordinary Shares (LSE:JET2), InterContinental Hotels Group (LSE:IHG), and International Consolidated Airlines Group SA (LSE:IAG) have all suffered a double whammy from higher oil prices and travel disruption.

Scenario 2: long-term conflict causes inflationary shock

If the conflict in the Middle East does escalate to boots on the ground and prolonged fighting, there are a number of clear outcomes for markets. Equity markets do not currently price in a long-term conflict and would be expected to drop at least a further 15-20% from current levels.

The two key factors would be a sharp rise in inflation, which would cause economic growth to slow, raising the prospect of stagflation.

Rajeev Sibal, senior global economist at investment bank Morgan Stanley, highlights that inflation usually passes through the system rapidly, taking only three months before growth begins to slow.

The team at Morgan Stanley expects that every $10 per barrel increase in the price of oil could result in inflation increasing around 0.30% in the United States, 0.40% across the Euro area, 0.30% in the UK, and 0.20% in China. Most of the current economic modelling was done with oil at around $70 per barrel, far below the current price at around $90 per barrel.

- Fund Focus: what the Iran conflict means for your portfolio

- Sector Screener: two stocks to consider amid market turmoil

- The funds capturing the oil price surge

Depending on domestic oil production levels, oil reserves and state policy, each government can adapt to how this inflationary shock impacts growth within the economy. The United States would see a limited impact on growth from higher oil prices, while the drop in GDP from every $10 per barrel increase in the oil price would be 0.15% in the Euro area, 0.10% in the UK, 0.10% in Japan and 0.30% in China, according to initial estimates from Morgan Stanley.

The other important element to watch is how long the oil price remains elevated above the $70 per barrel that most of the current economic forecasts were completed. When Russia invaded Ukraine, it initially claimed the “special military operation” would take 10 days, we are now into the fifth year of hostilities.

In this scenario, investors would want to look at defensive options such as oil majors BP (LSE:BP.), and Shell (LSE:SHEL) and gold exchange-traded funds. A more complex shipping picture with rising prices should also help London-based ship brokers Clarkson (LSE:CKN) and Braemar (LSE:BMS). Given markets are still near all-time highs, raising some cash would be a good option.

Tailored approach

The issue right now is that there is a lot of noise about record oil prices and falling share prices, but longer term the market has taken a more measured approach. Forewarned is forearmed in this case and it would be foolish to decide on a headline.

Each investment decision should be made with a view to an individual’s ultimate goal and time horizon. While capital preservation is the starting point for all decisions, an investor soon approaching retirement would likely make different decisions to one with an investment horizon over five years who can ride out the ups and downs. As with all serious conflict the immediate impact is shocking and uncertain, but understanding what is already priced in and what the options are ensures a solid platform for making better decisions.

John Ficenec is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.