Shares for the future: a new candidate for the Decision Engine

There’s a company with a very good financial track record that analyst Richard Beddard has been itching to cover. But the outcome’s ‘heartbreaking’. Here’s why.

27th February 2026 15:04

by Richard Beddard from interactive investor

This week I’m introducing a new candidate for the Decision Engine. It’s an itch I can’t stop scratching and I’m hoping that publishing will release me from my compulsion.

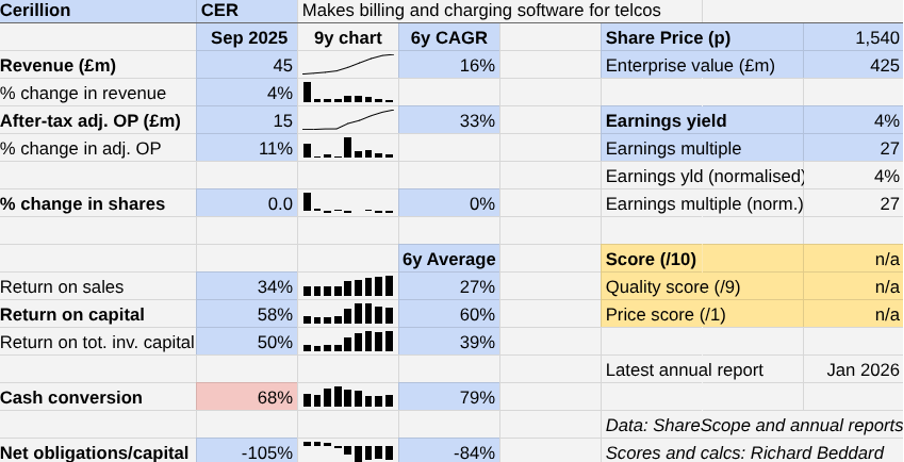

That company is Cerillion (LSE:CER). I am trying to reconcile its very good financial track record with a heavy dose of uncertainty.

- Invest with ii: Open an ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Cerillion: improving on good

Cerillion was born when it spun out of Logica in 1999. Louis Hall, who is still chief executive, led the management buyout. It listed on AIM in March 2016.

Since 2017, its first full year as a listed firm, the company has grown revenue and profit at a double-digit compound annual growth rate (CAGR), while earning high return on capital and generating strong cash conversion.

There’s been an improvement in revenue growth, and an even more impressive increase in profit growth since 2020. Cerillion develops software for telecommunications companies. It allows them to create tariffs and packages, and bill and charge customers for mobile, landline, TV and internet usage.

Cerillion profits when it sells software licences and charges for services to implement and customise the software. Licence revenue is more profitable than service revenue because there’s very little cost associated with it. Services require engineers and developers to tinker with the software.

Cerillion says its performance has improved as the size of customers has increased. Larger customers require more licences, but service revenues don’t increase proportionally. The latest modular iterations of its products are less work to implement, they can be modified remotely, and offer more off-the-shelf features, reducing the contribution of less profitable service work.

- Ian Cowie: are you braced for AI apocalypse or buying into AI optimism?

- ii Tech Focus: Nvidia, software stocks, Crowdstrike, Broadcom

I don’t think Cerillion is in the big league though, given the customers that it names are not all UK household names. In 2021, it contracted with Telasur, Suriname’s only full-service telecommunications company. In 2022, it contracted with Cable & Wireless Seychelles. In 2025, though, it won a £25.3 million contract with an "existing European customer" and implemented software for Virgin Media Ireland.

Since Cerillion appears to have experienced a step change in profitability, I have used the last six years of data to calculate growth, profitability and the normalised earnings multiple.

While profit margin continued to improve in the year to September 2025, the rapid revenue growth streak stuttered as revenue edged up 4%. Cerillion said it did not convert record orders into contracts, raising the expectation that some of this revenue will be secured in 2026.

The consensus of analysts’ forecasts is a 16% revenue increase in 2026, so perhaps 2025 was a blip.

On the face of it, Cerillion is a very appealing prospect. It has a cash surplus and has grown entirely under its own steam. The accounts are devoid of exceptional adjustments, barring the initial IPO costs and a head office move years ago.

Revenue risk

A decline in cash conversion over the last three years may be concerning though. It has fallen below 70% from 100% or more. This shortfall in cash flow relative to profit results from growing receivables - money owed by customers but not yet paid to Cerillion. Cerillion explains this is the result of mismatches between when it is paid and when revenue is recognised (and profit is booked) in the accounts.

For straightforward implementations, licences and services are recognised as soon as the customer has the right and ability to use the software. In the case of complex installations, licences and services are often bundled together and paid when performance milestones relating to software implementation are reached. These implementation periods can last over a year. The recognition of revenue from services smoothly tracks the work done by the company rather than the lumpier performance milestones.

- Eight FTSE 100 stocks to pay £6bn of dividends in March

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

I wonder if receivables have also increased as more customers choose to use software hosted in the cloud. Cerillion’s revenue recognition policy allows for revenue from hosted software to be recognised upfront if the customer could legally and practically install the software locally. It seems likely Cerillion is paid over the contract term.

I cannot judge whether this complex accounting brings revenue and profit forward, flattering Cerillion’s growth rates and profitability levels. It is recognised as a key accounting issue by the auditor who gave the accounts a clean bill of health in 2025.

Another factor contributing to the cash shortfall is capitalised development expenditure, which increased markedly in 2025 as Cerillion developed artificial intelligence (AI) tools and composable user interfaces for its products. Composable user interfaces are modular and can be easily reconfigured.

Some of this cost was treated as an investment and recognised as an asset on the company’s balance sheet, rather than a cost deducted from profit. The cost will be amortised over a number of years, spreading the impact on profit out. The software developers were, of course, paid so the full cost was deducted from cash flow.

Future shock!

Along with the rest of the software industry, Cerillion is transitioning from a permanent licence model to SaaS (Software as a Service), a rental model where the software is maintained and upgraded centrally, paid for by subscription and accessed through a web browser.

The allure of SaaS for customers is that it reduces the cost and hassle of ownership. The allure to software companies is more reliable revenue. The allure to me is that it would simplify the accounting.

The transition appears to be at an early stage. Cerillion sells one product that charges a subscription. That product, Skyline, is in part of a Managed Services division that contributes 9% of perhaps SaaS-like subscription revenue. Recurring revenue in 2025 was 35%, but the company's definition of recurring revenue goes way beyond software subscriptions.

Skyline, incidentally, is not part of the core telecommunications suite. It is a billing and charging platform for any subscription or usage-based service.

- Rolls-Royce shares surge again on stunning results

- ii view: new Diageo strategy involves massive dividend cut

The SaaS transition can disrupt businesses. In the short term it reduces or eliminates revenue and profit growth because upfront licence payments are replaced by subscriptions spread out over the contract term.

As the transition completes though, growth should, other things being equal, reassert itself as each new subscription builds on the recurring revenue from existing ones.

Bespokeness may be what made Cerillion special, though. Licences are most profitable, but services make the software more sticky. Cerillion earns 82% of revenue from its top 10 customers and 29% of revenue from the largest. The duration of a software licence is typically five years, but customers typically stay with Cerillion for at least 10.

This embeddedness may be challenged by SaaS because part of its appeal is ease of deployment and configuration. Transition to a SaaS model could make it easier for customers to switch, although Cerillion believes that vulnerability is with rivals whose products are more bespoke.

The new wild card in software is AI. Customers can already use the Large Language Model of their choice to create tariffs and packages and query billing information. As software developers incorporate AI to make their products easier to use and configure, this may intensify the commodification and fungibility of software more.

I have been touched by the AI scare that has spooked traders and sent the prices of software and data companies reeling in recent weeks. Curiously, Cerillion is not one of them. Its share price values the enterprise at a handsome 27 times normalised profit.

My fears run deeper. Tallying up my uncertainties; accounting complexity, weakened cash flow, a potentially disruptive SaaS transition, and the unknowable impact of AI, I feel unable to score Cerillion now, which is heartbreaking.

I would like to be braver. Perhaps there’s a reader who can tell me why I should be.

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

company | description | score | qual | price | ih% | |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.0 | 0.8 | 9.6% | |

2 | Hollywood Bowl | Operates tenpin bowling centres | 8.0 | 0.6 | 7.2% | |

3 | Howden Joinery | Supplies kitchens to small builders | 8.0 | 0.5 | 7.0% | |

4 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | |

5 | Softcat | Sells software and hardware to businesses and public sector | 7.5 | 0.9 | 6.9% | |

6 | Bunzl | Distributes essential everyday items consumed by organisations | 7.5 | 0.6 | 6.2% | |

7 | Jet2 | Flies people to holiday locations, often on package tours | 7.0 | 1.0 | 6.0% | |

8 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 7.5 | 0.5 | 6.0% | |

9 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 0.9 | 5.8% | |

10 | Auto Trader | Online marketplace for motor vehicles | 7.0 | 0.9 | 5.7% | |

11 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | 0.2 | 5.4% | |

12 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | |

13 | Keystone Law | Operates a network of self-employed lawyers | 7.5 | -0.1 | 4.7% | |

14 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 0.8 | 4.6% | |

15 | Judges Scientific | Manufactures scientific instruments | 7.0 | 0.3 | 4.6% | |

16 | Porvair | Manufactures filters and laboratory equipment | 8.0 | -0.7 | 4.5% | |

17 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.6 | 4.2% | |

18 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | 0.1 | 4.2% | |

19 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | |

20 | Macfarlane | Distributes and manufactures protective packaging | 6.0 | 1.0 | 4.0% | |

21 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 1.0 | 3.9% | |

22 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.7 | 3.7% | |

23 | Volution | Manufacturer of ventilation products | 8.5 | -1.7 | 3.5% | |

24 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.5 | 3.0% | |

25 | Goodwin | Casts and machines steel and processes minerals for niche markets | 8.5 | -2.2 | 2.6% | |

26 | Anpario | Manufactures natural animal feed additives | 7.0 | -0.8 | 2.5% | |

27 | Tristel | Manufactures hospital disinfectant | 8.0 | -2.1 | 2.5% | |

28 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -1.8 | 2.5% | |

29 | 4Imprint | Customises and distributes promotional goods | 8.0 | -2.4 | 2.5% | |

30 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -1.3 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.