Share Sleuth: how this trio of trades came to pass

Given his desire to keep the portfolio near fully invested in equities, Richard Beddard explains how he decided what to buy and what to trim.

12th November 2025 09:35

by Richard Beddard from interactive investor

Before I made any trades this month, Share Sleuth had more than £20,000 in cash, enough to fund four trades at the minimum trade size of 2.5% of the portfolio’s total value.

Since my objective is to keep Share Sleuth near fully invested in shares, my focus was on adding shares. An extraordinary increase in Goodwin (LSE:GDWN)’s share price meant, try as I might, I couldn’t avoid liquidating some of what had become the portfolio’s biggest holding, though.

- Invest with ii: Top UK Shares | Share Tips & Ideas | Cashback Offers

Additions: FW Thorpe and Bloomsbury

As well as ranking shares, the Decision Engine uses a share’s score to suggest its ideal holding size. The higher the score, the bigger the holding size.

If a holding deviates from its ideal holding size by more than 2.5% of the Share Sleuth portfolio’s total value (the minimum trade size) the Decision Engine suggests a trade.

The highest-ranked share available to the portfolio was the highest-ranked share in the Decision Engine, Thorpe (F W) (LSE:TFW). Adding shares was a no-brainer as I had just scored them.

Although I reduced the portfolio’s holding in FW Thorpe in 2015, it has held shares in the company continuously since 2010.

Hollywood Bowl Group (LSE:BOWL), an operator of tenpin bowling centres in the UK and Canada, YouGov (LSE:YOU), the market research firm, and Bloomsbury Publishing (LSE:BMY) were also highly ranked and available to the portfolio.

I passed on YouGov, which isn’t a member of the Share Sleuth portfolio, because publication of its annual report was imminent, and the company has been through a turbulent couple of years. I thought it best to wait until I had re-evaluated the share.

I also passed on Hollywood Bowl, because I added shares in October and I prefer to move slowly.

Bloomsbury made me pause for thought.

Last month, the publisher published half-year results. It expects adjusted profit before tax for the full year to February 2026 to be higher than prior forecasts of £41.6 million. Since the company earned £42 million in profit in the full year to February, the numbers suggested profit will grow somewhat.

These numbers are difficult to interpret because of Bloomsbury’s wild card, Sarah J. Maas. The launch of a new title from the blockbuster author at the end of Bloomsbury’s 2024 financial year had a big impact on profit in 2024 and 2025. Although the company followed up with the softback this summer, the absence of a new title would, other things being equal, have been expected to lead to contraction in profit this year.

- Outlook for 2026: why more records could be broken

- Stockwatch: an AIM share now going up through the gears

On the face of it, news of growth is reassuring. But a contributor to the forecast 2025 outcome is another wild card, this time in Bloomsbury’s academic and professional division.

The company has licensed some of its content to an artificial intelligence (AI) partner, which is not exclusive, and dependent on authors opting in to the arrangement.

Reportedly, opting in earns a one-off payment for the author. After the work is incorporated into the AI’s training data there will be no further payments. The Society of Authors has criticised this aspect of the deal (as well as the size of the authors’ cut).

Bloomsbury declined to comment when I asked whether its revenues from the deal would also be one-off in nature, so I think it is safest to assume they are. To my mind, that reduces its significance over the long term, and further complicates our understanding of the company’s performance in the short term.

That said, I didn’t see any reason to change my score, which recognises AI as a risk already. Bloomsbury must work out how to defend its authors’ rights and profit from AI. This is part of the process.

Share Sleuth has held Bloomsbury shares since 2019. I have twice reduced the holding size, in 2022 and 2024.

On Tuesday 4 November, I added 1,037 more shares in Bloomsbury at a price just shy of 496p and 1,791 more shares in FW Thorpe at 287p. After deducting £10 for each trade in lieu of broker fees, the total cost of each was about £5,150, Share Sleuth’s minimum trade size on the day.

Reductions: Goodwin

Goodwin’s re-rating caught me by surprise. I thought one day the company would be worth as much as the stock market ascribes to it, but not this month! By 4 November, the share price had risen 140% since I last reduced the holding in August and 280% since the previous time I took profit, in August 2024.

The extraordinary popularity of Goodwin shares is not hard to rationalise. In October, the company announced that it expects profit to double in the year to April 2026 reflecting strong performances across the business and a pivot into manufacturing parts for the nuclear and defence industries, a decision taken a decade or so ago that seems more than prescient in hindsight.

Because of their size and the advanced alloys used in their construction, these parts require a large foundry and specialist expertise to manufacture, capabilities few Western companies have. Contracts to supply containers for spent nuclear fuel and submarine programmes could run for decades.

- Stockwatch: a FTSE 100 recovery buy or falling growth star?

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

The company may have an ace up its sleeve too. A new business, Duvelco, manufactures a high-performance polyamide (plastic), Ducoya. Goodwin has suggested Duvelco might one day become its biggest business, and it is expected to start contributing revenue in the next financial year (2026-27). Today, it is only contributing to costs.

I don’t usually use forecasts, but this one comes directly from the company, which has made good on its promises so far. The price score makes no sense without it. I rescored Goodwin using the forecast outcome for the current year.

I also increased Goodwin’s score for how capably it has made money by half a point to the maximum, 3. Having created new capabilities it has demonstrated it can profit from them. Essentially, I’m overlooking modest revenue growth and cash conversion over the past decade because Goodwin has reached another level and the future is unlikely to be like the recent past.

That was as accommodating as I could be. My summary looked like this:

Goodwin | GDWN | Casts and machines steel and processes minerals for niche markets | 04/11/2025 | 6.5/10 |

How capably has Goodwin made money? | 3.0 | |||

Over the last six years, family-run Goodwin has grown revenue modestly and profit in the low double-digits, while building capacity and capabilities in niche markets new and old. In 2026, profit is expected to double. Heavy capital expenditure has reduced cash conversion in the past, but the company is seeing the benefits now. | ||||

How big are the risks? | 2.5 | |||

Contracts with military and nuclear customers are lumpy but secure and diverse revenue streams insulate Goodwin from variations in any one business. Its chair and two managing directors are family members, representing generations of experience. New projects often take longer than expected to commercialise. | ||||

How fair and coherent is its strategy? | 3.0 | |||

The company has maintained decent levels of profitability while proving it can develop new markets, justifiably raising expectations of growth and confirming its long-term ethos. It has trained a highly skilled workforce, employee retention is high and the directors pay themselves a relatively modest 10 times the median income of £46,000. | ||||

How low (high) is the share price compared to profit? | -2.0 | |||

High. A share price of 23,100p values the enterprise at £1,759 million, about 31 times forecast profit. | ||||

NB: Bold text indicates factors that reduce the score. Bold and italicised text doubly so. The maximum score is 3 for each criterion except price, which has a maximum of 1 (explainedhere) | ||||

Nearly all the risk is in the share price, as I see it, which before I made these changes relegated Goodwin to the bottom of the Decision Engine table. Now it is a few places higher.

Even after my changes, Goodwin’s score evaluated to an ideal holding size of just 2.9% of the portfolio’s total value. The share price had gone up so far, so fast, Share Sleuth’s Goodwin holding was worth 9.1% of its total value. The difference was 6.2%.

I decided to take some profit, but I couldn’t bring myself to go the whole hog. I last reduced the holding less than three months ago, and I don’t like to rush. Second, I’m trying to work the portfolio back up to being fully invested, and reducing Goodwin all the way would have put more of the portfolio in cash - despite the addition of FW Thorpe and Bloomsbury shares.

On 4 November, I reduced Share Sleuth’s Goodwin holding by 23 shares at a price of £231.25. The transaction raised £5,309, after deducting £10 in lieu of broker fees.

Share Sleuth scores

As we move into November/December, the most under-represented Decision Engine Shares are Softcat (LSE:SCT) (ranked 7), Hollywood Bowl (ranked 8), and Judges Scientific (LSE:JDG) (ranked 9). These are prime candidates for investment. Judges Scientific is not currently a member of the Share Sleuth portfolio.

Goodwin remains the only share that is over-represented. The price has fallen back a bit since I reduced the holding but it still accounts for 6.1% of the portfolio. The Decision Engine tells me the holding should be 3.4%, a difference of 2.7% (more than the minimum trade size of 2.5%).

0 | company | description | score | qual | price | ih% | ss% |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.7 | 9.0 | 0.7 | 9.5% | 8.9% |

2 | Howden Joinery | Supplies kitchens to small builders | 8.0 | 0.6 | 7.3% | 5.9% | |

3 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | 6.0% | |

4 | Bunzl | Distributes essential everyday items consumed by organisations | 7.5 | 0.5 | 6.1% | 4.6% | |

5 | Jet2 | Package tour operator and leisure airline | 7.0 | 1.0 | 6.0% | 5.3% | |

6 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 1.0 | 5.9% | 3.6% | |

7 | Softcat | Sells hardware and software to businesses and the public sector | 8.0 | -0.2 | 5.6% | 2.4% | |

8 | Hollywood Bowl | Operates tenpin bowling centres | 7.5 | 0.2 | 5.3% | 2.6% | |

9 | Judges Scientific | Manufactures scientific instruments | 7.5 | 0.1 | 5.1% | ||

10 | Porvair | Manufactures filters and laboratory equipment | 8.0 | -0.4 | 5.1% | 3.5% | |

11 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | 2.6% | |

12 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 1.0 | 5.0% | 4.5% | |

13 | Renew | Maintenance and improvement of national infrastructure | 7.5 | -0.1 | 4.7% | 6.0% | |

14 | Auto Trader | Online marketplace for motor vehicles | 8.0 | -0.7 | 4.6% | ||

15 | 4Imprint | Customises and distributes promotional goods | 8.0 | -0.7 | 4.6% | 1.9% | |

16 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | -0.3 | 4.5% | 4.8% | |

17 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.6 | 4.2% | 2.1% | |

18 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | 2.4% | |

19 | Macfarlane | Distributes and manufactures protective packaging | 6.0 | 1.0 | 4.0% | 2.6% | |

20 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | -0.1 | 3.9% | ||

21 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.6 | 3.9% | 5.0% | |

22 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 0.8 | 3.7% | ||

23 | Keystone Law | Operates a network of self-employed lawyers | 7.5 | -0.8 | 3.5% | ||

24 | Goodwin | Casts and machines steel and processes minerals for niche markets | 8.5 | -1.8 | 3.4% | 6.1% | |

25 | Anpario | Manufactures natural animal feed additives | 7.0 | -0.3 | 3.3% | 2.9% | |

26 | Volution | Manufacturer of ventilation products | 8.0 | -1.4 | 3.3% | ||

27 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.5 | 3.0% | 2.0% | |

28 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -0.3 | 2.5% | 3.9% | |

29 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -1.7 | 2.5% | 2.2% | |

30 | Tristel | Manufactures disinfectants for simple medical instruments and surfaces | 7.5 | -2.1 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio, ss% is the actual size of Share Sleuth’s holding, and ih%-% is the difference between ideal and actual sizes.

Softcat has published its annual report, so my decision will depend on the score I give it shortly. Hollywood Bowl’s annual report should follow shortly after in January, and since I’ve traded it recently I’m unlikely to consider it again until then.

Judges Scientific needs some thought. Since I scored it in May, Judges has published half-year results and I’ve finally begun to accept the medium and even long-term prospects for international exporters may have diminished.

I’m currently re-scoring YouGov, which was a candidate this time, but has provisionally dropped to 22nd place. Volution Group (LSE:FAN) has also published its annual report and is due to be re-scored.

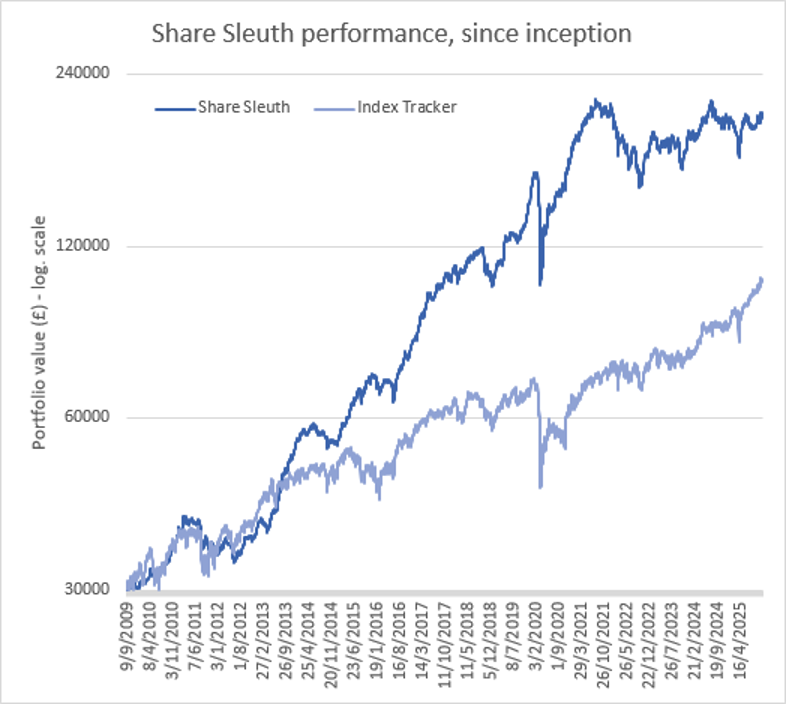

Share Sleuth performance

At the close on Friday 7 November, Share Sleuth was worth £200,855, 570% more than the £30,000 of pretend money we started with in September 2009.

The same amount invested in accumulation units of a FTSE All-Share index tracking fund would be worth £104,237, an increase of 248%.

Share Sleuth, 09 Nov 2025 | Cost (£) | Value (£) | Return (%) | ||

Cash (8% of portfolio) | 16,593 | ||||

Current holdings (23 shares) | 184,262 | ||||

Total, and performance since 9 September 2009 | 30,000 | 200,855 | 570 | ||

Benchmark: FTSE All-Share index tracker (acc) | 30,000 | 104,327 | 248 | ||

Companies | Shares | Cost (£) | Value (£) | Return (%) | |

AMS | Advanced Medical Solutions | 1,965 | 4,503 | 4,185 | -7 |

ANP | Anpario | 1,124 | 4,057 | 5,789 | 43 |

BMY | Bloomsbury | 1,882 | 8,354 | 9,617 | 15 |

BNZL | Bunzl | 417 | 9,798 | 9,216 | -6 |

BOWL | Hollywood Bowl | 1,972 | 4,971 | 5,305 | 7 |

CHH | Churchill China | 1,495 | 17,228 | 5,233 | -70 |

CHRT | Cohort | 326 | 1,118 | 4,062 | 263 |

FOUR | 4Imprint | 116 | 2,251 | 3,770 | 67 |

GAW | Games Workshop | 66 | 4,116 | 10,098 | 145 |

GDWN | Goodwin | 58 | 1,403 | 12,296 | 777 |

HWDN | Howden Joinery | 1,476 | 10,371 | 11,904 | 15 |

JET2 | Jet2 | 822 | 5,211 | 10,587 | 103 |

LTHM | James Latham | 1,150 | 14,437 | 12,075 | -16 |

MACF | Macfarlane | 7,689 | 10,011 | 5,182 | -48 |

OXIG | Oxford Instruments | 505 | 10,044 | 9,019 | -10 |

PRV | Porvair | 906 | 4,999 | 6,940 | 39 |

QTX | Quartix | 1,618 | 3,988 | 4,320 | 8 |

RNWH | Renew Holdings | 1,310 | 9,804 | 11,960 | 22 |

RSW | Renishaw | 234 | 6,227 | 7,921 | 27 |

SCT | Softcat | 326 | 4,992 | 4,828 | -3 |

SOLI | Solid State | 5,009 | 6,033 | 7,263 | 20 |

TFW | Thorpe (F W) | 6,153 | 14,861 | 17,844 | 20 |

TUNE | Focusrite | 2,020 | 14,128 | 4,848 | -66 |

Notes

Costs include £10 broker fee, and 0.5% stamp duty where appropriate

Cash earns no interest

Dividends and sale proceeds are credited to the cash balance

Objective: To beat the index tracking fund handsomely over five year periods

Source: ShareScope.

After the trades and dividends paid during the month from Advanced Medical Solutions Group (LSE:AMS), Churchill China (LSE:CHH), Jet2 Ordinary Shares (LSE:JET2) and Macfarlane Group (LSE:MACF), Share Sleuth has £16,593 in cash.

The minimum trade size, 2.5% of the portfolio’s value, is just over £5,000.

Past performance is not a guide to future performance.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns all the shares in the Share Sleuth portfolio.

For more on the Share Sleuth portfolio, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.