Shares for the future: second chance for Decision Engine reject?

After being relegated from his 30-strong list of companies last year, analyst Richard Beddard revisits this share to see if it’s good enough to re-enter the table.

20th February 2026 15:00

by Richard Beddard from interactive investor

When I scored Treatt (LSE:TET)last year, it was a mixed bag. Demand for flavour ingredients in the years since the pandemic had been erratic. Subsequent events though, led me to eject the company from the Decision Engine and liquidate Share Sleuth’s holding.

- Invest with ii: Open a Stocks & Shares ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Treatt’s customers are mainly global flavour houses and beverage companies. They had overstocked during the pandemic and subsequently destocked, making the long-term revenue trend difficult to interpret. But in 2024, the company said conditions had normalised and revenue was at a record high.

Profit had increased for the third consecutive year, although it was still below its 2021 peak, when customers were buying more than they needed (in hindsight). Treatt had grown profit at a modest 5% compound annual growth rate (CAGR) since its highest pre-pandemic profit in 2018.

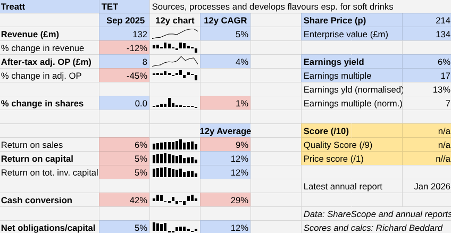

Return on Capital, though, had fallen well below pre-pandemic levels to 10%. Treatt had not yet capitalised on “generational” investments in a factory, laboratory and headquarters in the UK.

The growth in operating capital, the investment in its factories primarily, had vastly outstripped the growth in profit.

The new UK site opened in September 2021 so, glass half-full, perhaps it was just a matter of time before automation and increased collaboration with clients was evident in return on capital.

Daemmon Reeve, the charismatic and long-serving chief executive who championed the investment, once told me the new HQ should contribute to higher profitability from year three, so perhaps good things would follow in 2025 and beyond.

There was a blemish in this hopeful vision though. In 2024, Reeve was no longer chief executive. He had resigned in October 2023 and left in December. The company’s long-standing chief financial officer, Richard Hope, had stepped down the year before.

Worst year in recent history

The hopeful vision was dashed in the year to September 2025, with David Shannon and Ryan Govender in the executive roles. They did not last as long as their predecessors. Govender left at the end of the financial year and Shannon shortly after.

Treatt’s interim managing director and chief financial officer is Manprit Randhawa. He joined the company as interim chief financial officer in September 2025, and he was confirmed as permanent CFO earlier this month. The search for a permanent CEO is ongoing.

In some ways the results are secondary to events in 2025, but the results were bad. Revenue declined 12% and adjusted after tax operating profit declined by 45%. Return on capital was just 5%, below the 8-10% range I consider to be prosperous even in bad years.

The company says weak demand in the US, where Treatt earned 40% of revenue, and high citrus prices, did the damage.

US demand fell due to weak consumer confidence and tariff uncertainty. High citrus prices encouraged customers to seek cheaper formulations, also reducing revenue.

Treatt also says that it took it longer to convert prospects into sales during the year. The uncertain economic conditions probably contributed, but maybe uncertainty about Treatt did too (I will come to that later).

Profit declined by more than revenue due to Treatt’s high fixed costs.

Ill winds hit Treatt’s biggest flavour category, citrus oils, which earned it 55% of revenue in 2025. They also hit at least two of its more profitable (“Premium”) categories: fruit and vegetables (8% of revenue) and Tea (6%).

Treatt is aiming to accelerate growth in the Premium category. But in 2025, Premium revenue fell by more than total revenue.

Throughout Treatt’s long history trading and refining citrus oils, raw material prices have driven swings in revenue and profitability. But these results may show that more novel and less price-sensitive flavours cannot be relied on to provide a stable income stream, if we drink fancy beverages in similar quantities when money is tight.

- Why fund managers are ‘uber-bullish’ despite AI concerns

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Profit declined more than revenue because the costs of Treatt’s manufacturing facilities are largely fixed. Costs, like depreciation, have increased considerably due to the new facilities.

The problem facing investors is whether the worst year at Treatt for a long time marks the failure of a strategy many years in the making, which is to earn more revenue from novel flavours addressing high-value sections of the beverage market. Or whether vindication has been delayed by the stop-go economic conditions of the post-pandemic era.

It would be easier to believe the hopeful vision were it not for the fact that the board seemed to lose confidence in the strategy.

Events, dear boy, events

The executives who championed the investment and resigned soon after they had delivered may have lost confidence, but I reserved my judgement. Daemmon Reeve and Richard Hope had each served Treatt for more than two decades, and both had expressed an interest in a quieter life.

Although I had already liquidated Share Sleuth’s holding by then, it was events in September 2025 that made me think management had lost confidence.

David Shannon had been chief executive for just over a year when the board recommended a takeover at a price that massively undervalued the company if my hopeful scenario was likely. The offer price was 260p, 16% more than Treatt’s share price the day before, and only a couple of months after Treatt’s share price had cratered due a trading update that foreshadowed this year’s results.

- Stockwatch: a trust that could continue to multiply

- The Analyst: defence – how to play the new tech sector

If Treatt’s capitulation was a surprise, so was the way the deal fell apart. The takeover was thwarted by Döhler, a German ingredients company and customer of Treatt. Treatt hasn’t disclosed the proportion of revenue from Döhler, but no customer contributed more than 10% of total revenue in 2025.

Döhler bought a 28% stake, enough to block the deal. It also creates a potential conflict of interest, which the two companies are managing through a relationship agreement.

The agreement gives Döhler a seat on the board (now occupied). It seeks to ensure that the two companies trade at arm’s length and confidential information is protected.

Curiously then, a customer had the most significant impact on Treatt’s strategy in 2025, by allowing it to continue. That is not particularly edifying.

I’m cheering team hopeful from the sidelines but before I recommit, and score Treatt again, I need to know who is running the company at least. More clarity will come with the appointment of a permanent chief executive, but I wonder how to gauge Döhler’s influence.

30 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score more than 5 out of 10 to be worthy of long-term investment in sizes determined by the ideal holding size (ihs%).

company | description | score | qual | price | ih% | |

1 | FW Thorpe | Makes lighting systems for commercial, industrial and public settings | 9.0 | 0.8 | 9.6% | |

2 | Hollywood Bowl | Operates tenpin bowling centres | 8.0 | 0.6 | 7.1% | |

3 | James Latham | Distributes imported panel products, timber, and laminates | 7.5 | 1.0 | 7.0% | |

4 | Howden Joinery | Supplies kitchens to small builders | 8.0 | 0.5 | 7.0% | |

5 | Softcat | Sells software and hardware to businesses and public sector | 7.5 | 0.9 | 6.8% | |

6 | Bunzl | Distributes essential everyday items consumed by organisations | 7.5 | 0.6 | 6.2% | |

7 | Jet2 | Flies people to holiday locations, often on package tours | 7.0 | 1.0 | 6.0% | |

8 | Renew | Maintains and improves road, rail, water, and energy infrastructure | 7.5 | 0.5 | 6.0% | |

9 | Solid State | Manufactures electronic systems and distributes components | 7.0 | 0.9 | 5.9% | |

10 | Auto Trader | Online marketplace for motor vehicles | 7.0 | 0.9 | 5.7% | |

11 | Bloomsbury Publishing | Publishes books and educational resources | 7.5 | 0.3 | 5.6% | |

12 | Churchill China | Manufactures tableware for restaurants etc. | 6.5 | 1.0 | 5.0% | |

13 | Oxford Instruments | Makes imaging and semiconductor manufacturing systems | 6.5 | 0.8 | 4.6% | |

14 | Judges Scientific | Manufactures scientific instruments | 7.0 | 0.3 | 4.6% | |

15 | Porvair | Manufactures filters and laboratory equipment | 8.0 | -0.8 | 4.5% | |

16 | Keystone Law | Operates a network of self-employed lawyers | 7.5 | -0.4 | 4.2% | |

17 | Cake Box | Cake shop franchise and sweet manufacturer | 7.0 | 0.1 | 4.2% | |

18 | Advanced Medical Solutions | Manufactures surgical adhesives, sutures and dressings | 6.5 | 0.6 | 4.1% | |

19 | Focusrite | Designs recording equipment, synthesisers and sound systems | 6.0 | 1.0 | 4.0% | |

20 | Macfarlane | Distributes and manufactures protective packaging | 6.0 | 1.0 | 4.0% | |

21 | YouGov | Surveys public opinion and conducts market research online | 6.0 | 1.0 | 3.9% | |

22 | Games Workshop | Designs, makes and distributes Warhammer. Licenses IP | 8.5 | -1.7 | 3.7% | |

23 | Volution | Manufacturer of ventilation products | 8.5 | -1.8 | 3.5% | |

24 | Cohort | Manufactures/supplies defence tech, training, consultancy | 8.0 | -1.4 | 3.2% | |

25 | Anpario | Manufactures natural animal feed additives | 7.0 | -0.9 | 2.5% | |

26 | Goodwin | Casts and machines steel and processes minerals for niche markets | 8.5 | -2.4 | 2.5% | |

27 | Tristel | Manufactures hospital disinfectant | 8.0 | -2.1 | 2.5% | |

28 | 4Imprint | Customises and distributes promotional goods | 8.0 | -2.4 | 2.5% | |

29 | Quartix | Supplies vehicle tracking systems to small fleets | 7.5 | -1.9 | 2.5% | |

30 | Renishaw | Makes tools and systems for manufacturers | 6.5 | -1.4 | 2.5% |

Click on a share's score to see a breakdown (scores may have changed due to movements in share price). Key: qual is the share’s score out of 9 for the three quality factors (capabilities, risks, and strategy), price is the price score from -3 to +1, and ih% is the suggested ideal holding size as a percentage of the total value of a diversified portfolio.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard holds many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine and Share Sleuth, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.